Japan

Country Overview

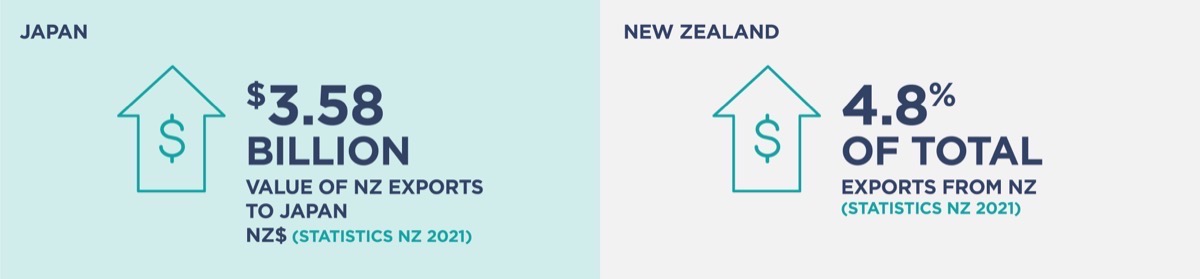

Japan is the world’s third largest economy behind the US and China. It’s our fourth largest export market, with dairy, fruit and aluminium New Zealand’s top exports to Japan.

An island nation roughly the size of New Zealand, Japan has 126 million inhabitants. It’s one of the world’s largest consumer markets and has a high proportion of millionaire households.

Japan’s ageing population presents significant business opportunities aimed at over-65s, including pre-prepared foods.

Japanese consumers have a keen eye for product quality and high expectations around service delivery, (sales, delivery, packaging, and after-sales support). E-commerce is well-developed in Japan with high user penetration.

Trade agreements

Japan is one of our most important trading and investment partners. The Comprehensive and Progressive Trans-Pacific Partnership (CPTPP) – a free trade agreement between 11 countries in the Asia-Pacific region – has greatly benefited New Zealand’s trade with Japan, giving our exporters preferential access into the market. Tariffs have been reduced or eliminated across every sector.

Country intelligence

The Robinson Country Intelligence Index is a holistic measurement of country-level risk and serves as an alternative measure of country development. It incorporates four broad dimensions of Governance, Economics, Operations and Society. A higher ranking indicates a better Country Intelligence Index score.

Value of New Zealand exports

International logistics performance

The International Logistics Performance Index measures how efficiently countries move goods across and within borders. Countries are ranked on their index score with a higher ranking indicating higher performance of trade logistics based on six components: customs, infrastructure, ease of international shipments, logistics services quality and competence, tracking and tracing, and timeliness.

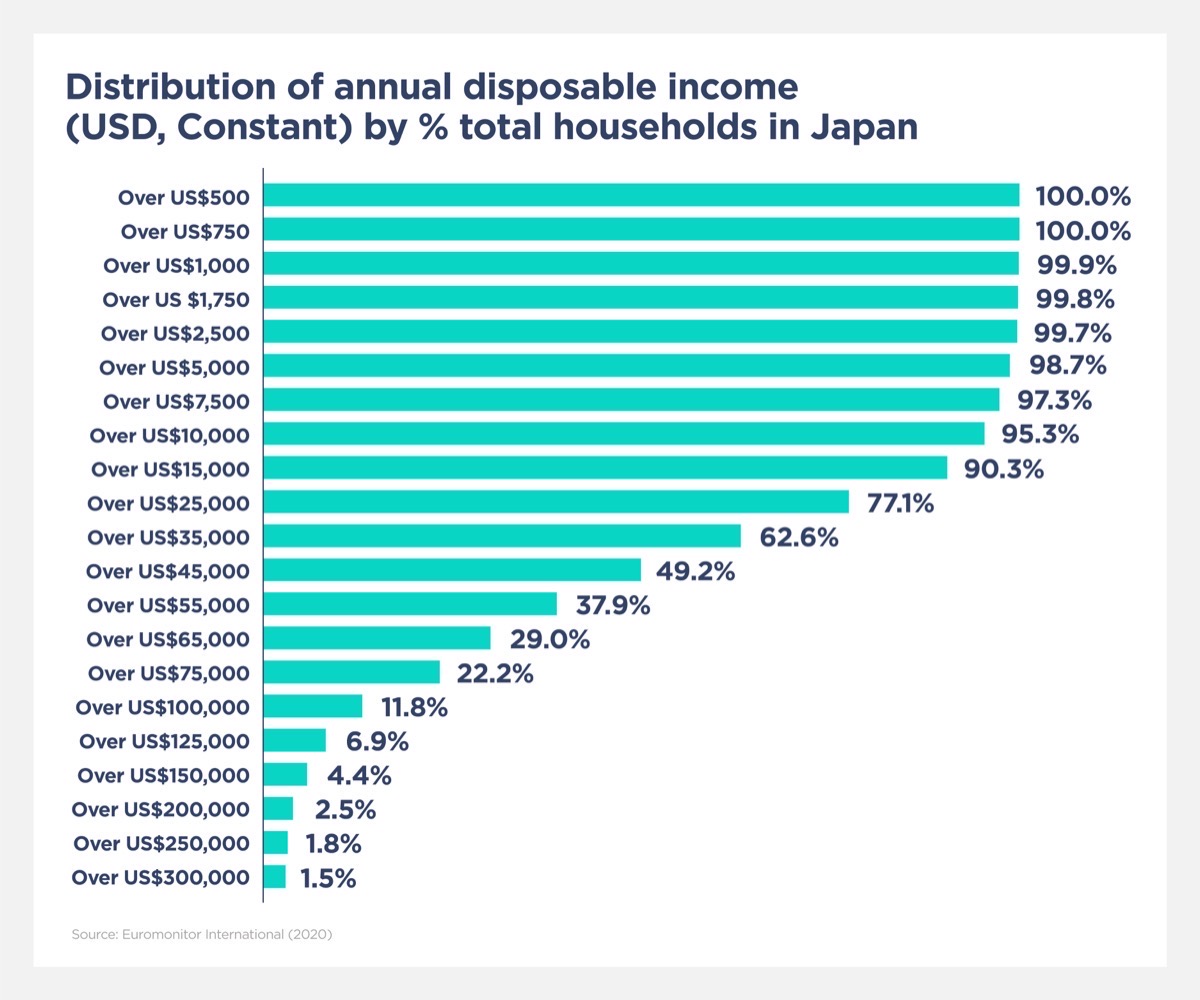

Income and distribution of wealth

Global National Income (GNI) per capita is the dollar value of a country's final income in a year, divided by its population.

Annual Disposable Income refers to gross income minus social security contributions and income taxes. Each income band presents data referring to the percentage of households with a disposable income over that amount.

Further information

For more information to validate Japan as an export market, see our Japan Market Guide.

- Vitamins & Dietary Supplements

- Skin Care

- Dog & Cat Food

- Alcoholic Drinks

- Health & Wellness Packaged Food & Beverages

Vitamins & Dietary Supplements

- Market size and growth

-

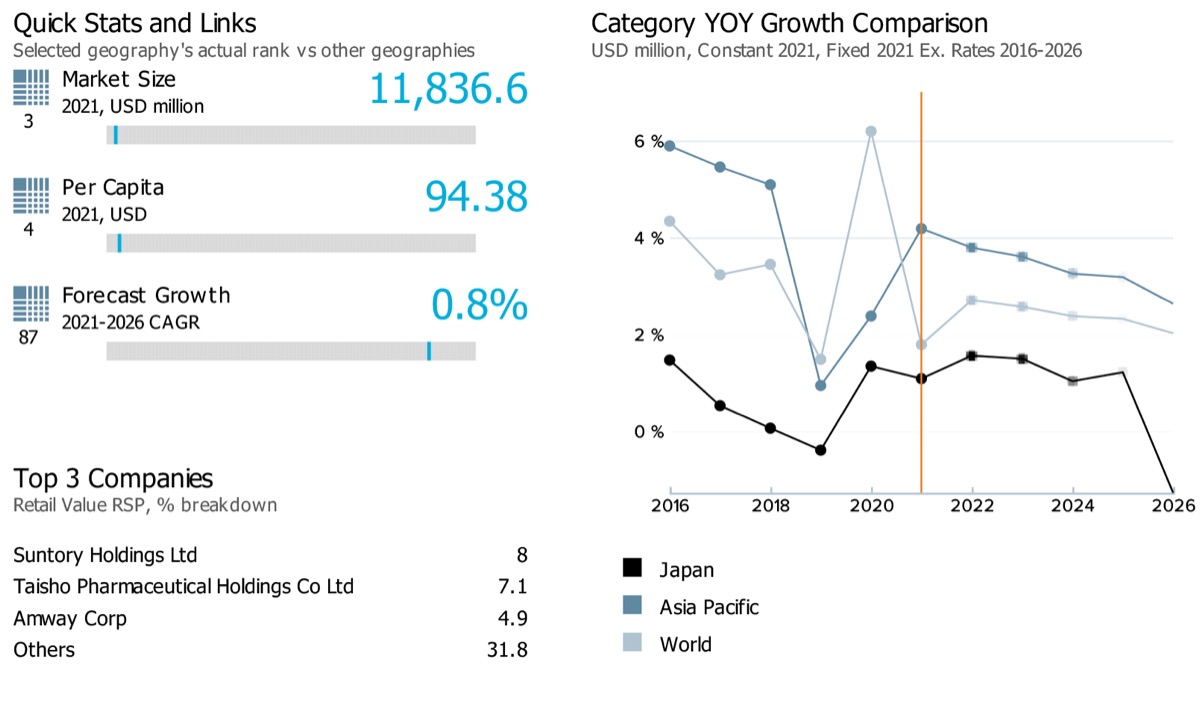

Note: Data on the top left corner of the image (3,4, and 87) showcases respective ranks for Japan for its market sizes, per capita, and forecast growth rate compared against 99 countries globally. The blue line on the grey bar represents the relative position of the country as per their rank.

Note: Latest market size data for the year 2021 has been shared for Vitamins & Dietary Supplements

Japan's retail value sales of vitamins and dietary supplements witnessed a historic compound annual growth of 0.9% during 2016-2021. It is expected to remain steady at a retail value CAGR of 0.8% over 2021-2026. Globally, the category is expected to witness a slow down from a historic CAGR of 5.1% to an estimated forecast CAGR of 2.4% over the same period for its retail value sales.

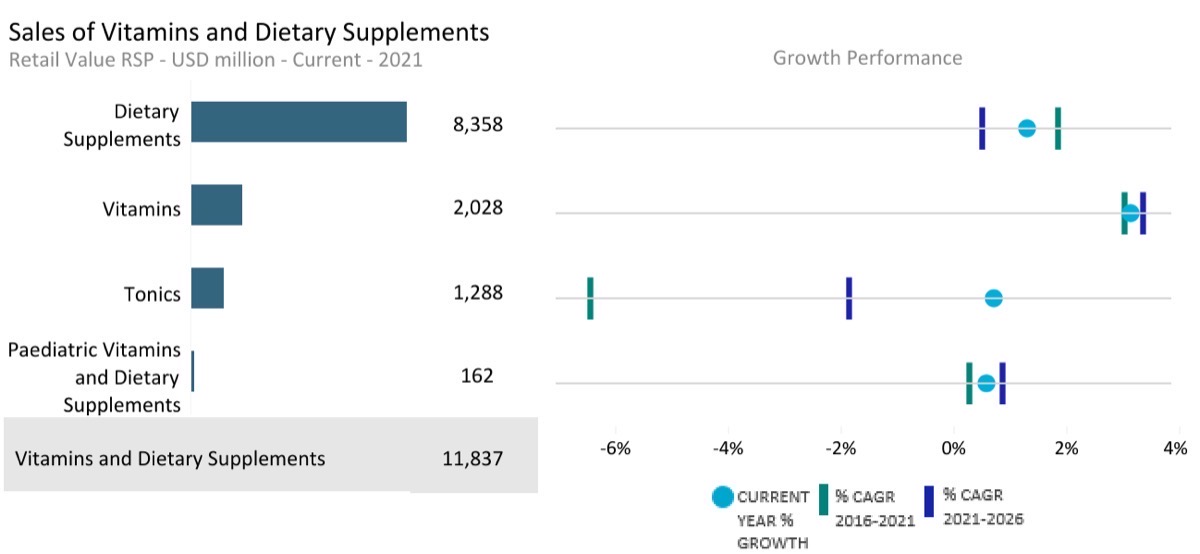

- Sub-category breakdown

-

Note: Current year growth in the above chart refers to the period 2021-22

Category

Unit

Market size (2021)

Retail value RSP

Forecast compound annual growth rate (2021/2026) %

Vitamins and Dietary Supplements

USD million

11,836.63

0.79

Vitamins

USD million

2,028.14

3.37

Paediatric Vitamins and Dietary Supplements

USD million

161.78

0.89

Dietary Supplements

USD million

8,358.45

0.51

Tonics

USD million

1,288.26

-1.86

- Channel distribution

-

Note: The chart here showcases the retail value share of different channel sales for Vitamins and dietary supplement products in Japan in 2021. The triangle/dash represents whether the specific channel share has increased/decreased or remained the same against its share in the previous year.

- Market Insights

-

Market trends

- COVID-19 has had a wide-reaching impact, from immediate concerns relating to the immune system to an indirect impact on the mental health of the consumers relating to issues like depression and anxiety. Within dietary supplements, those products which helped address the above issues have witnessed the strongest performances. Ginseng, for example, is well-known for its immune-system-boosting properties and being a potent antioxidant that can help reduce inflammation. As such, some consumers have stocked up on ginseng to help them prepare for COVID-19.

- In line with the above trend, increased sales of Vitamin C and Vitamin D, both well-known for their immune-boosting effects, have continued. On the other hand, multivitamins remain the most popular segment as consumers look for a convenient approach to guarantee enough vitamins to battle the pandemic. Furthermore, with many consumers focused on their immune system, sales of some other vitamins which are less well-known for their benefit have suffered, including vitamin B and vitamin E.

Prospects and growth opportunity

- Dietary supplements have become an encouraging category for smaller players to enter because of increasedconsumer health awareness and the expanding range of their potential functionalities. As a result, new products, formats and services are frequently being introduced, which might bode well for the growth of dietary supplements over the coming years. For example, tapping into the burgeoning FemTech trend, Dricos Inco launched Fem Server in December 2019 which is a personalised supplement subscription service for women which changes the combination based on the consumer’s condition.In addition, demand for items that support healthy ageing, such as those that assist bone and heart health and brain capability, are predicted to grow rapidly.

- Despite competition from other products like dietary supplements, vitamins are still viewed as having potential, especially given the heightened health concerns created by COVID-19. In addition to this, Vitamin C has also been positively impacted by its growing association with skin care. An increasing number of consumers looking for solutions to skin problems or simply desiring a fair and clear complexion have turned towards vitamin C.

General health & wellness trends

- Vitamins are generally viewed as medication by consumers. This has discouraged them from using such products for long periods. However, vitamins manufacturers have worked to differentiate vitamins from medicines by developing novel formats, most notably the gummy format.

- Personalisation is a key theme across many industries in Japan and it already exists within dietary supplements. More players are expected to enter this sphere over the forecast period with it offering strong opportunities to add value to what is a relatively mature area of consumer health.

Skin Care

- Market size and growth

-

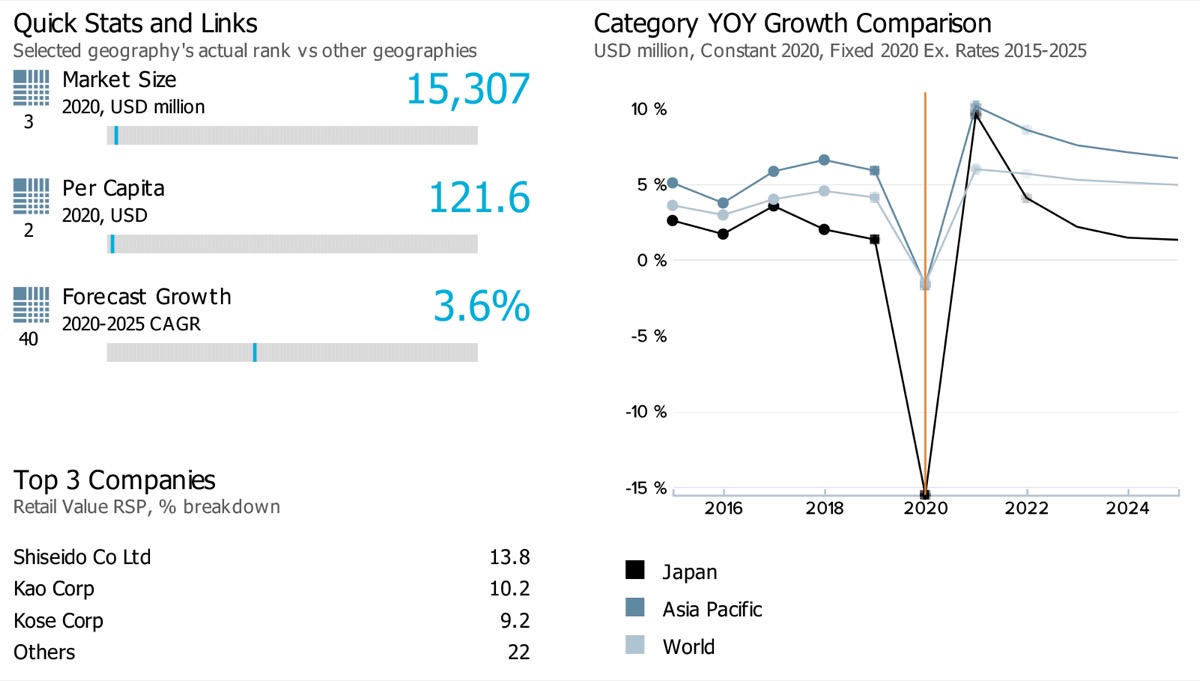

Note: Data on the top left corner of the image (3,2 and 40) showcases respective ranks for Japan for its market sizes, per capita, and forecast growth rate compared against 99 countries globally. The blue line on the grey bar represents the relative position of the country as per their rank.

Retail value sales of skin care products in Japan is expected to witness a rise in its compound annual growth rates, from -1.4% during 2015-2020 to 3.6% over 2020-2025. Similarly the category is estimated to witness an increased CAGR globally from 4.7% during 2015-2020 to 5.3% over 2020-2025

- Sub-category breakdown

-

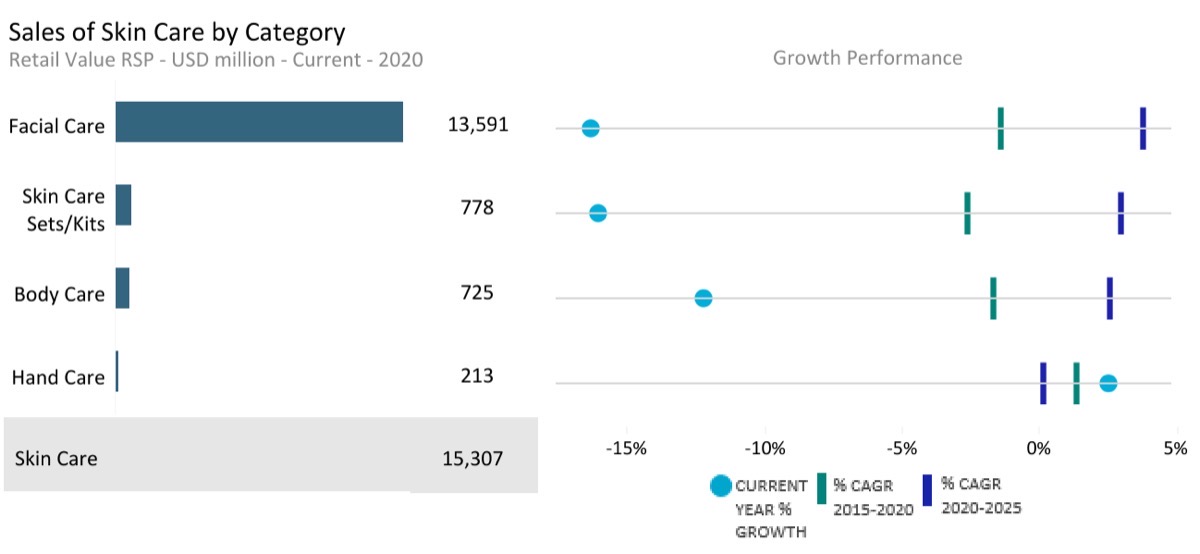

Note: Current year growth in the above chart refers to the period 2019-20

Category

Unit

Market size (2020)

Retail value RSP

Forecast compound annual growth rate (2020/2025) %

Skin Care

USD million

15,306.97

3.64

Body Care

USD million

724.93

2.56

Facial Care

USD million

13,591.45

3.78

Hand Care

USD million

212.77

0.18

Skin Care Sets/Kits

USD million

777.82

3.01

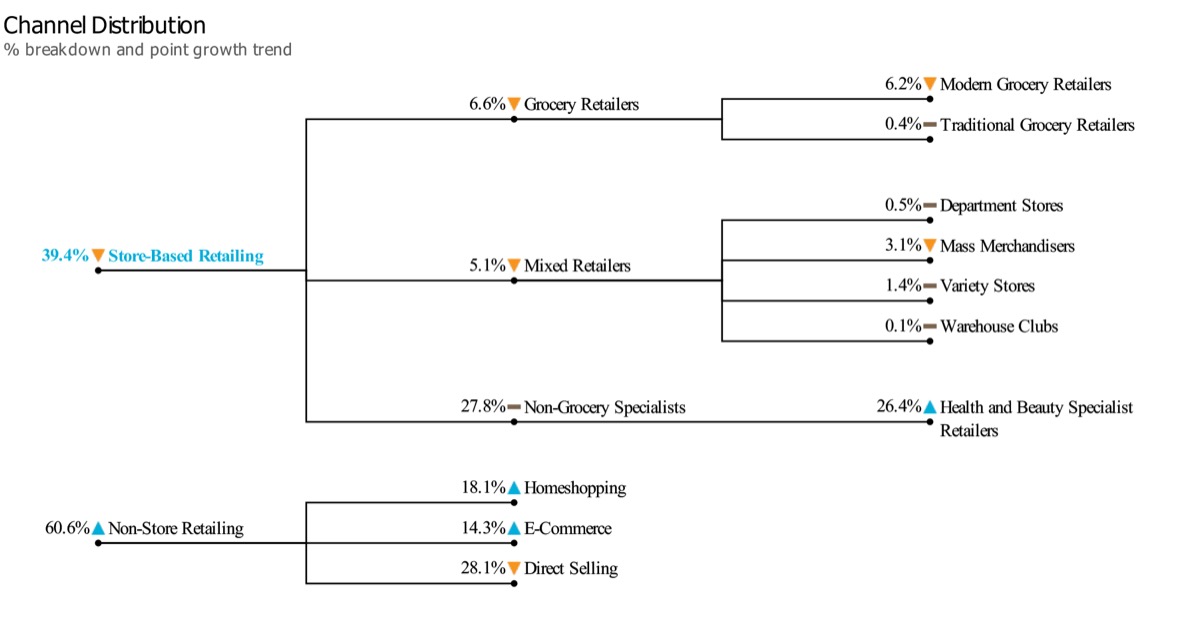

- Channel distribution

-

Note: The chart here showcases the retail value share of different channel sales for skin care products in Japan in 2020. The triangle/dash represents whether the specific channel share has increased/decreased or remained the same against its share in the previous year.

- Market Insights

-

Market trends

- Skin care products were less affected by the COVID-19 crisis than other beauty and personal care areas in 2020. The lack of social contact resulting from home seclusion and the shift to remote working had less of an impact than for categories such as colour cosmetics. This is mainly because skin care products play a central role in consumers’ daily personal care regimen.

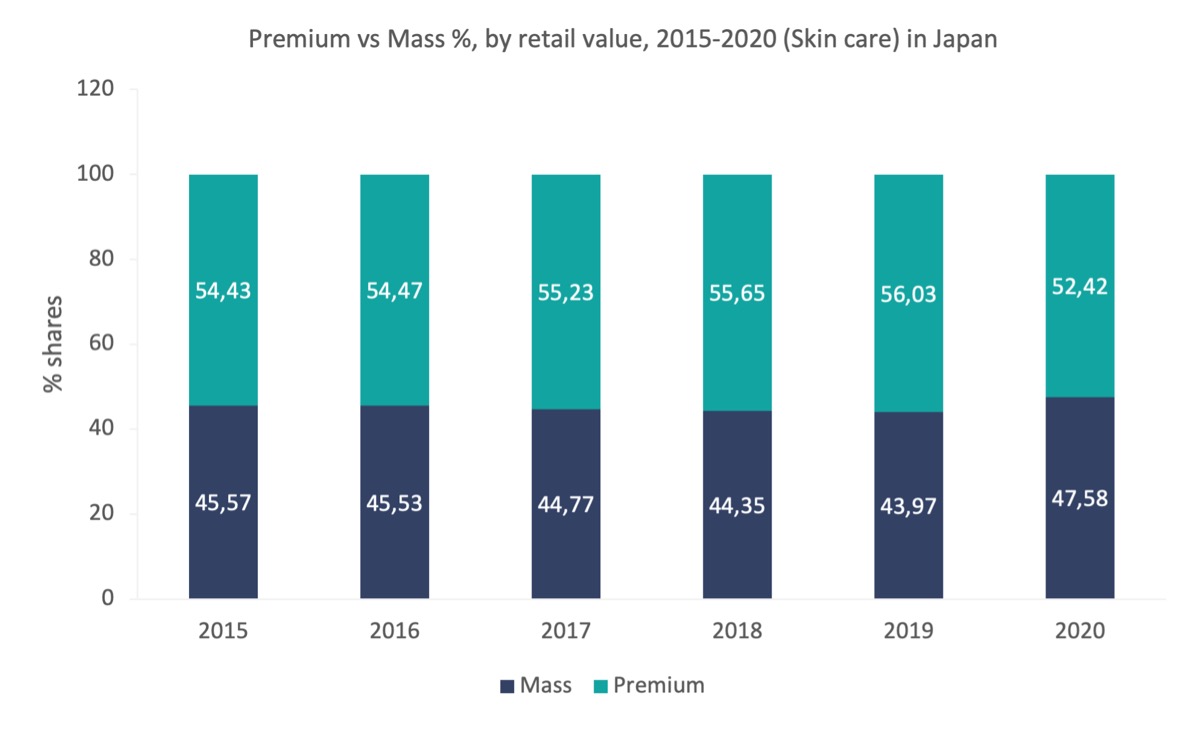

- However, COVID-19 has adversely affected the premium skin care segment by reducing the opening hours of beauty specialist retailers and department stores which represent key distribution channels in the segment.

- The COVID-19 crisis also witnessed an increased frequency of handwashing and the use of alcohol-based hand sanitisers due to concerns of viral infection. This has led to a rise in skin problems on consumers’ hands, which in turn, resulted in increased demand for hand care products such as hand cream.

Prospects and growth opportunity

- The pandemic is expected to have a lasting impact, both through the fall in inbound tourism and the economic consequences of measures introduced to contain COVID-19. This is expected to be a constraint on premium skin care’s recovery. The pandemic has also brought consumers’ health concerns to the fore, which has accelerated the shift towards a focus on safety and protection in beauty and personal care solutions. In addition, consumers spending more time at home during the pandemic looked to relieve stress and boredom by pampering themselves more, therefore, the dermo-cosmetics category is well-positioned to cater to consumers seeking targeted self-care solutions and products with more advanced functionality and greater efficacy.

- COVID-19 also led to restrictions on activities like customer service and product testing in department stores. This served to accelerate the development of leading brands’ efforts to engage with consumers online through actions such as non-contact skin diagnosis. This trend is likely to continue even as consumers feel confident returning to stores due to its convenience.

General health & wellness trends

- The competitive landscape within skin care continued to become increasingly fragmented in 2020 as new players from other industries looked to develop a presence in the category. For example, entertainment/production company, Stardust Group, launched a line of skin care called Sophistance in December 2019, which is inspired by traditional Japanese skin care treatments. While new players continued to disrupt the market, existing players looked to reorganise and revamp their portfolios to stay relevant. For example, leading player, Shiseido, discontinued its D'ici là brand in November 2019, while Kanebo Cosmetics Inc announced that it would be ceasing production of its Chicca brand. Trimming down their portfolios helps companies to focus on more profitable lines and to introduce new products.

- Anti-agers are expected to continue to be a notable area of development during the forecast period. This is primarily supported by Japan’s rapidly ageing population with 28.7 % of the population over 65 years of age. Consumers are becoming increasingly interested in products that can help them look and feel younger for longer.

Dog & Cat Food

- Market size and growth

-

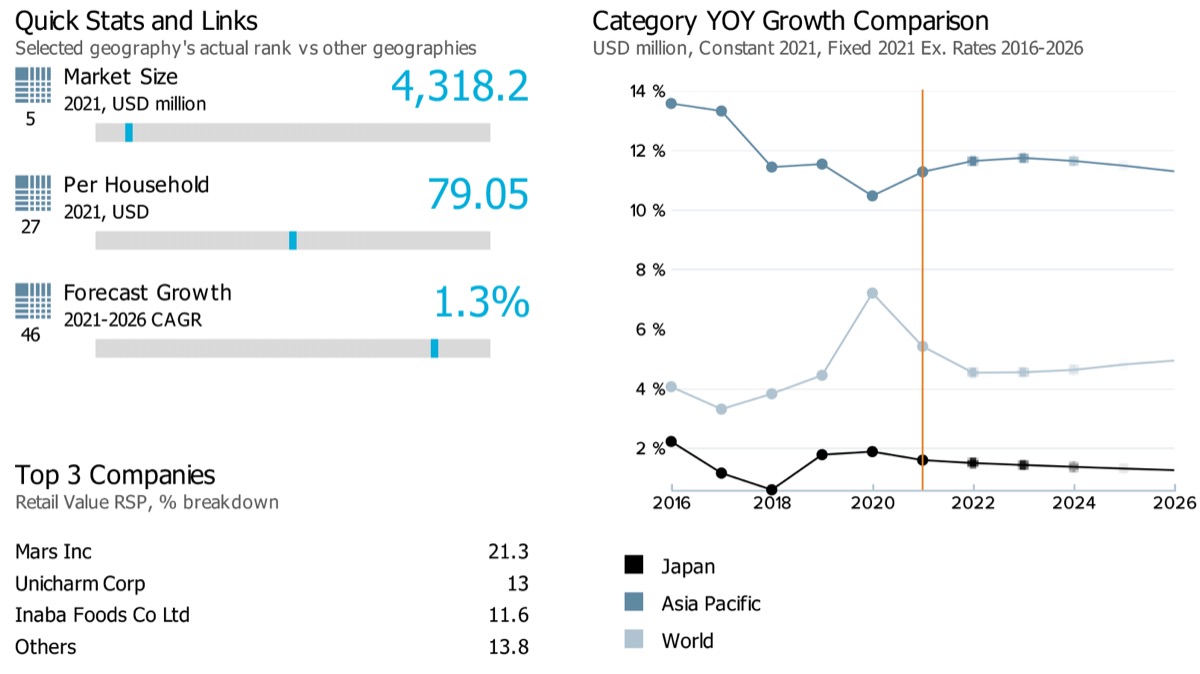

Note: Data on the top left corner of the image (5,27, and 46) showcases respective ranks for Japan for its market size, per capita, and forecast growth rate compared against 53 countries globally. The blue line on the grey bar represents the relative position of the country as per their rank.

Note: Latest market size data for the year 2021 has been shared for Dog and Cat food

In Japan, retail value sales of dog and cat food are estimated to slow down from a historic compound annual growth rate of 1.8% during 2016-2021 to an estimated forecast CAGR of 1.3% over 2021-2026. The category’s performance in the country has been slightly slower than its global performance. Globally, the category witnessed a historic CAGR of 6.9% and an estimated forecast CAGR of 4.7% during the same period.

- Sub-category breakdown

-

Note: Current year growth in the above chart refers to period 2020-21

Category

Unit

Market size (2021)

Retail value RSP

Forecast compound annual growth rate (2021/2026) %

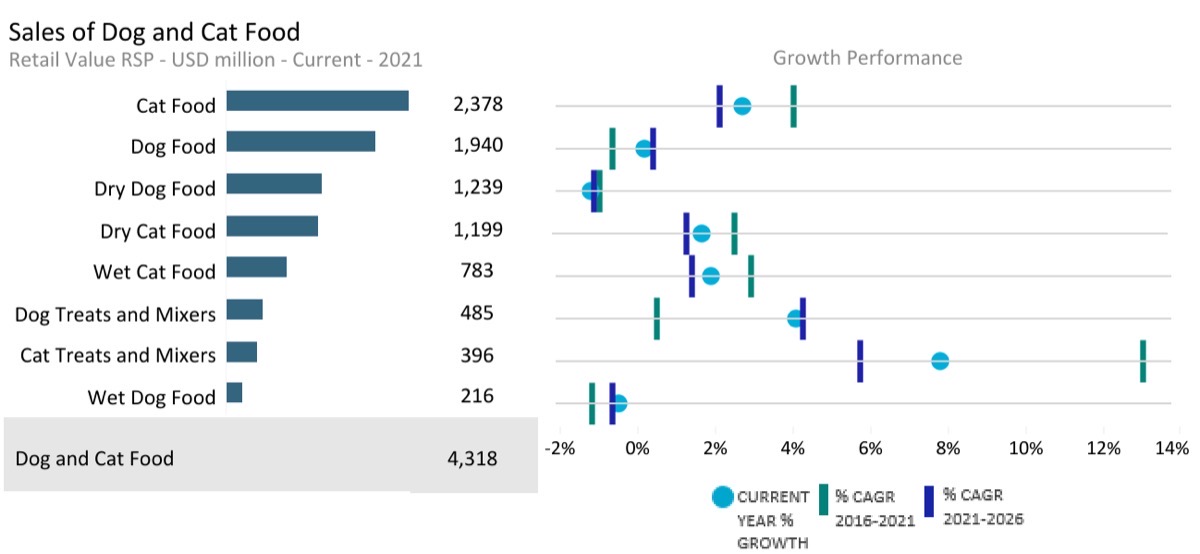

Dog and Cat Food

USD million

4,318.18

1.35

Dog Food

USD million

1,939.95

0.39

Dog Treats and Mixers

USD million

485.38

4.26

Dry Dog Food

USD million

1,238.70

-1.11

Wet Dog Food

USD million

215.87

-0.65

Cat Food

USD million

2,378.23

2.10

Wet Cat Food

USD million

782.88

1.42

Dry Cat Food

USD million

1,198.94

1.24

Cat treats and mixers

USD million

396.40

5.74

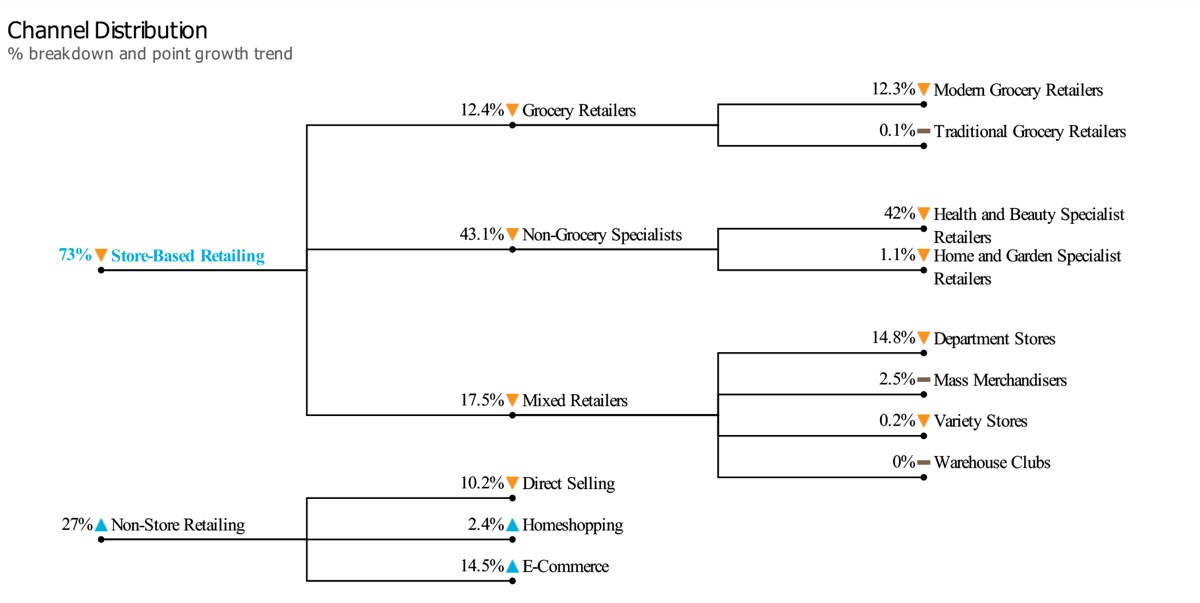

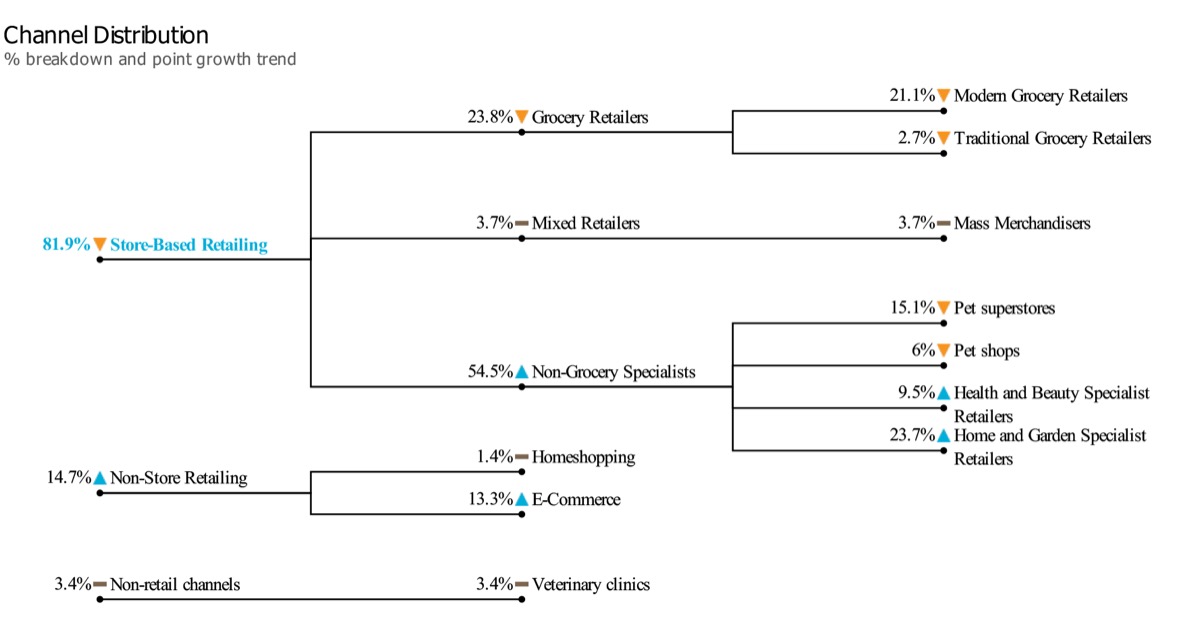

- Channel distribution

-

Note: The chart here showcases the retail value share of different channel sales for dog and cat food products in Japan in 2021. The triangle/dash represents whether the specific channel share has increased/decreased or remained the same against its share in the previous year

- Market Insights

-

Market trends

- Dog food in Japan continues to witness a decline in retail volume terms in 2021, primarily because of the decline in the dog population. In Japan, the overall dog population decreased in 2020, with consumers lacking the time, space, or energy to take care of a dog. However, the limited space available in typical urban households increases demand for smaller animals, including cats.

- Japanese consumers are willing to spend more money on their pets, supported by the rise in dual-income households and the country’s falling birth rate. In addition to this, the developing pet humanisation trend is also leading to consumers increased health awareness towards their pets, which has contributed positively to the sales of pet food in the country.

Prospects and growth opportunity

- Premium therapeutic dog food and dog treats are expected to remain a dynamic category within the dog food segment over the coming years. As the risk of disease increases with dogs' age, the demand for premium therapeutic dog food is also likely to grow. In addition, dog treats and mixers are also expected to perform well in 2021, with home seclusion resulting in consumers giving their dogs treats more often.

- Although not as developed as therapeutic dog food, premium therapeutic cat food is an area with plenty of opportunities. This is due to an increase in the average life expectancy of cats because of advancements in veterinary services and the availability of higher quality food. Also, there is still plenty of room for innovation and expansion for cat treats and mixers in terms of variety and price range, as these products are looking to attract a wide range of consumers.

General health & wellness trends

- Supplements are expected to continue growing as consumers look up to these products to maintain their pets’ health. As a result, it will be hard for manufacturers to maintain volume sales; moreover, under mounting pressure to deliver added-value products, it will be challenging to sustain their profit margins.

- There is also growing segmentation within dog food in general, with products targeting different breeds and different age groups. This helps manufacturers manage the volume sales issue, with products targeting smaller breeds in smaller pack sizes.

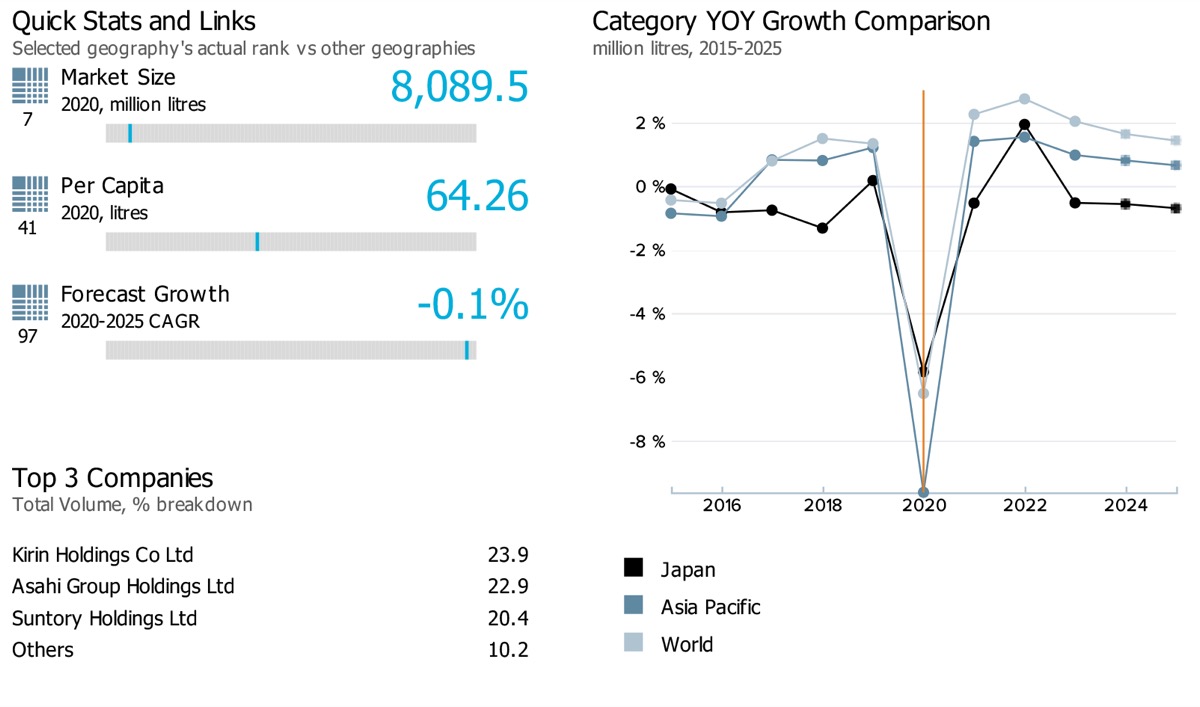

Alcoholic Drinks

- Market size and growth

-

Note: Market size data for the alcoholic drinks category in the country reflects the total volume in million litres. Data on the top left corner of the image (7,41 and 97) showcases respective ranks for Japan for its market size, per capita, and forecast growth rate compared against 99 countries globally. The blue line on the grey bar represents the relative position of the country as per their rank.

The compound annual growth rate for alcoholic drinks in Japan, both in terms of total value and volume, is expected to gain momentum over the forecast period (2020-2025: FCAGR for total value: 2.6% and for total volume: -0.1% ) against its performance in the historic period (2015-2020: HCAGR for total value: -4.1% and for total volume: -1.8% ). This is mainly in line with the category’s performance at the global level, where both in terms of total value and volume, alcoholic drinks are expected to gain momentum over the forecast period (2020-2025: FCAGR for total value: 4.6% and for total volume: 2.0% ) against its performance in the historic period (2015-2020: HCAGR for total value: 0.9% and for total volume: -0.7% )

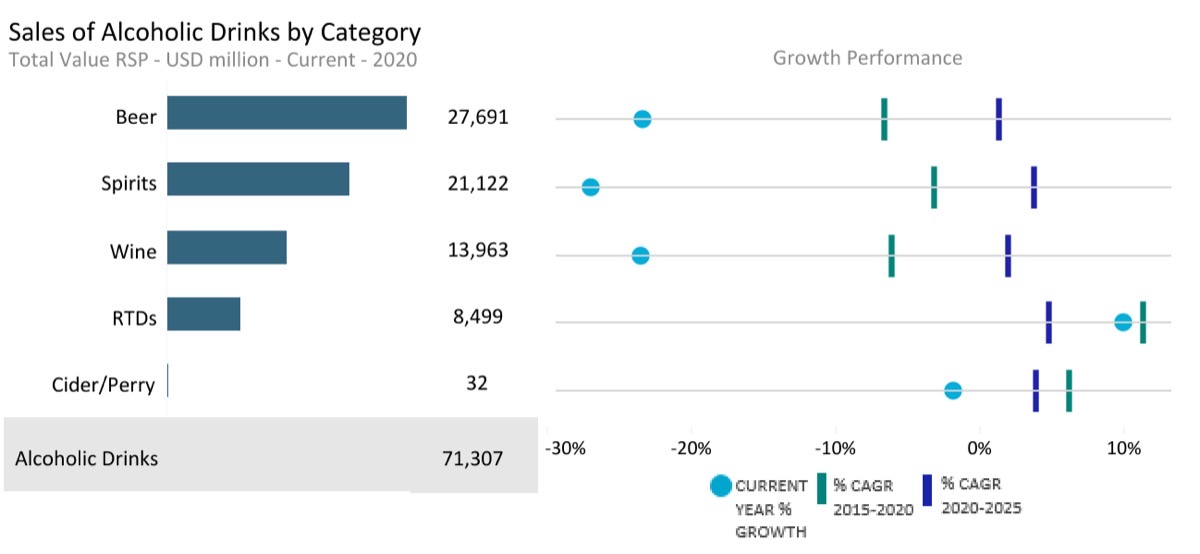

- Sub-category breakdown

-

Current year growth in the above chart refers to the period 2019-20

Category

Data type

Market size (2020)

USD million

Forecast compound annual growth rate (2020/2025) %

Alcoholic Drinks

Total Value RSP

71,307.03

2.64

Alcoholic Drinks

Off-trade Value RSP

40,869.05

-0.88

Alcoholic Drinks

On-trade Value RSP

30,437.98

6.73

Beer

Total Value RSP

27,690.85

1.33

Beer

Off-trade Value RSP

19,086.52

-2.82

Beer

On-trade Value RSP

8,604.33

8.68

Cider/Perry

Total Value RSP

32.03

3.87

Cider/Perry

Off-trade Value RSP

21.58

2.79

Cider/Perry

On-trade Value RSP

10.45

5.97

RTDs

Total Value RSP

8,498.97

4.75

RTDs

Off-trade Value RSP

8,184.18

4.67

RTDs

On-trade Value RSP

314.79

6.87

Spirits

Total Value RSP

21,122.13

3.82

Spirits

Off-trade Value RSP

7,462.08

-1.86

Spirits

On-trade Value RSP

13,660.05

6.47

Wine

Total Value RSP

13,963.04

2.01

Wine

Off-trade Value RSP

6,114.69

-2.25

Wine

On-trade Value RSP

7,848.34

4.89

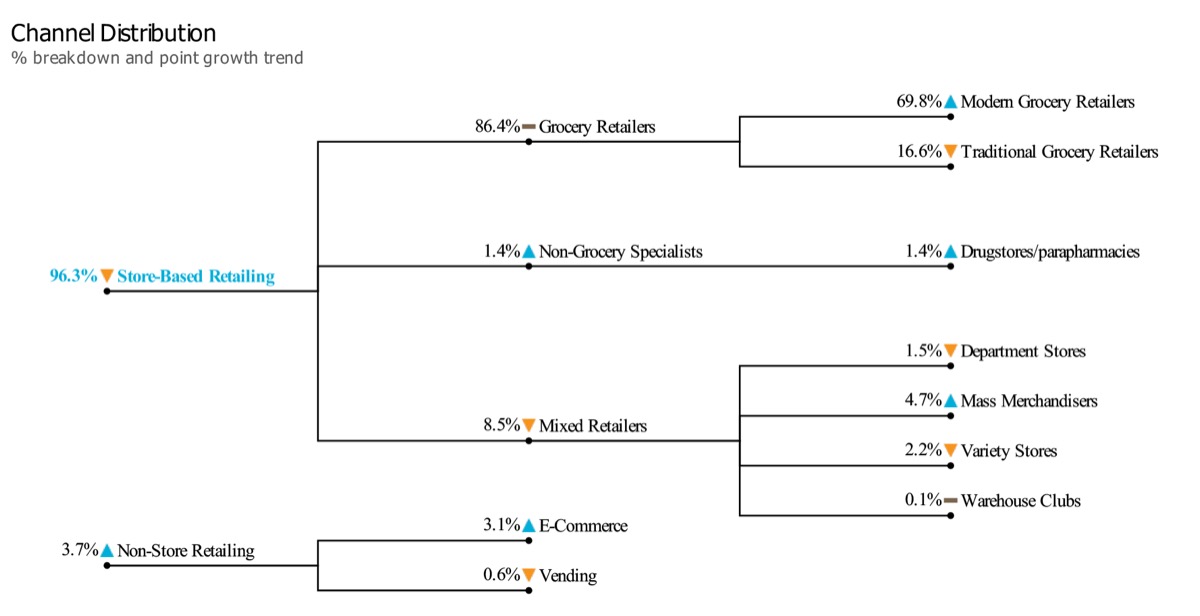

- Channel distribution

-

Note: The chart here showcases the off-trade volume share of different channel sales for alcoholic drink products in Japan in 2020. The triangle/dash represents whether the specific channel share has increased/decreased or remained the same against its share in the previous year

- Market Insights

-

Market trends

- COVID-19 had a catastrophic impact on the on-trade alcoholic drinks market in Japan throughout 2020. The country witnessed a marked shift in alcoholic drinks consumption from foodservice channels to home. As a result, the performance of alcoholic drinks categories was largely reliant on home consumption and off-trade channels. Overall, economy products performed well while premium to mid-priced products struggled, reflecting the considerable reliance of these segments on on-trade sales.

- With the first stage of the reformation of the liquor tax regime, 2020 was expected to be the year of recovery for beer. However, the impact was considerably diluted by the COVID-19 crisis. Economy beer, especially the so-called new genre beer, witnessed growing demand. On the other hand, premium and mid-priced beer witnessed significant declines because of the lack of drinking draught beer at foodservice venues. Some restaurants started to replace draught beer with a bottled beer in response to the strong drop in its demand.

- In the case of spirits, the sales performance of categories depended mainly on whether products were focused primarily on off-trade or on-trade channels. Brands such as Torys recorded strong growth, largely to their positioning as home drinking brands. On the other hand, Hibiki, Yamazaki and Hakushu witnessed a decline in sales because of premiumisation and huge dependence on on-trade channels. In addition, while increasingly drinking at home, consumers started to look for new products to inject a sense of novelty into their day-to-day experiences. The new product launched by Suntory was timely in this sense.

Prospects and growth opportunity

- The alcoholic drinks market is expected to witness new product launches adapted to the demands of the “new normal”. However, consumer lifestyles are still evolving rapidly post 2020 and remain largely unpredictable. Therefore, it is likely that manufacturers will launch products in beta versions to enable them to collect consumers’ feedback and improve the products. Consequently, the prominence of such development cycles is likely to increase during the forecast period.

- Guilt-free products will continue to witness increased demand during the forecast period. The health and wellness trend will be a major influence on consumer demand across a wide range of product areas, including beer. Health-oriented products such as Food with Functional Claims (FFC) labelled non-alcoholic beer, and low-carb or zero-carb beer is expected to remain popular. Such products respond to the conflicting demands of consumers, who wish to enjoy indulgence but are, at the same time, concerned about their health.

General industry trends

- Non-alcoholic drinks innovation is expected to extend from beer to other categories such as RTDs. Ethical consumerism is expected to be a growing trend in response to the increasing consumer awareness of the environment and social issues. Ethical products such as gin that tackles food waste by using surplus beer or sake lees in production, and organic wine that appeals to eco-conscious consumers should gain more attention. In addition, social alcohol-related problems, like alcohol addiction, will also gain attention, which will make it difficult for manufacturers to focus on products like RTDs with high alcohol content.

- In February 2021, the Japan Spirits & Liqueurs Makers Association announced standards for the labelling of Japanese whisky. Due to the lack of any standards, there had been cases of brands that only use imported foreign whisky being sold as “Japanese whisky” or cases where brands that do not meet the qualification of “whisky” under the Japanese liquor tax law being sold as “whisky” in other countries. The clear standards, in force from April 2021, are expected to maintain and enhance the reputation of Japanese whisky. This would, in turn, help promote the category’s further development in the form of increased sales during the forecast period.

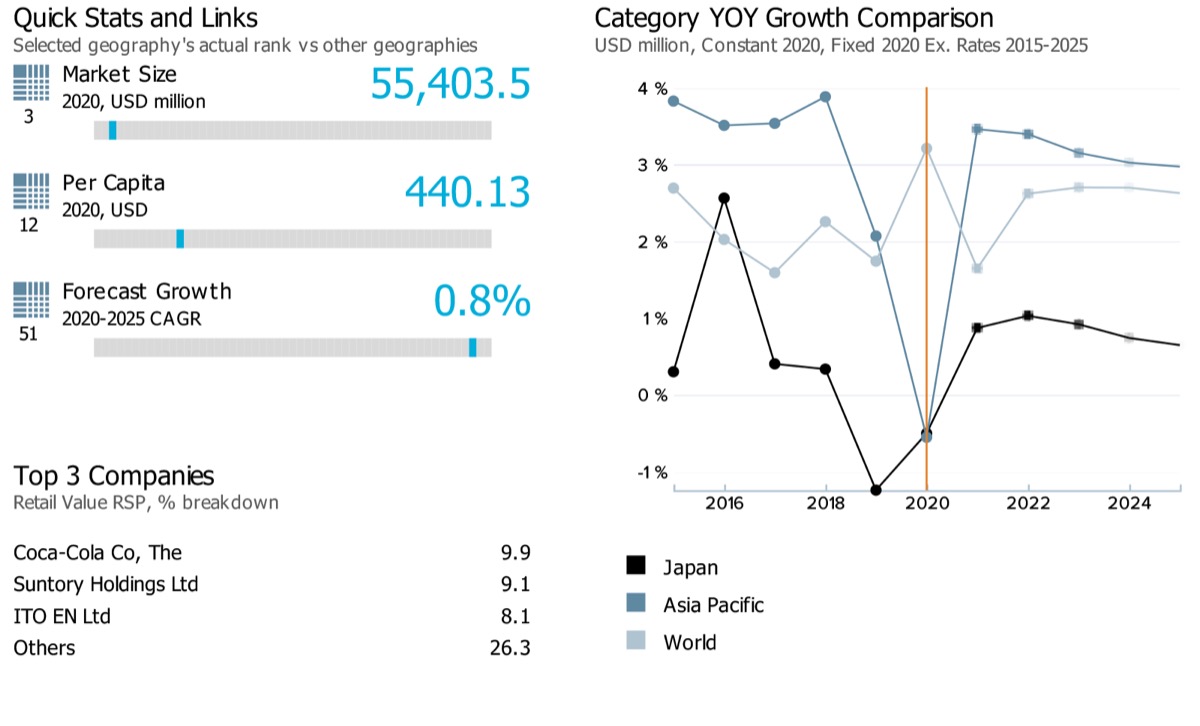

Health & Wellness Packaged Food & Beverages

- Market size and growth

-

Note: Data on the top left corner of the image (3,12 and 51) showcases respective ranks for Japan for its market sizes, per capita, and forecast growth rate compared against 53 countries globally. The blue line on the grey bar represents the relative position of the country as per their rank.

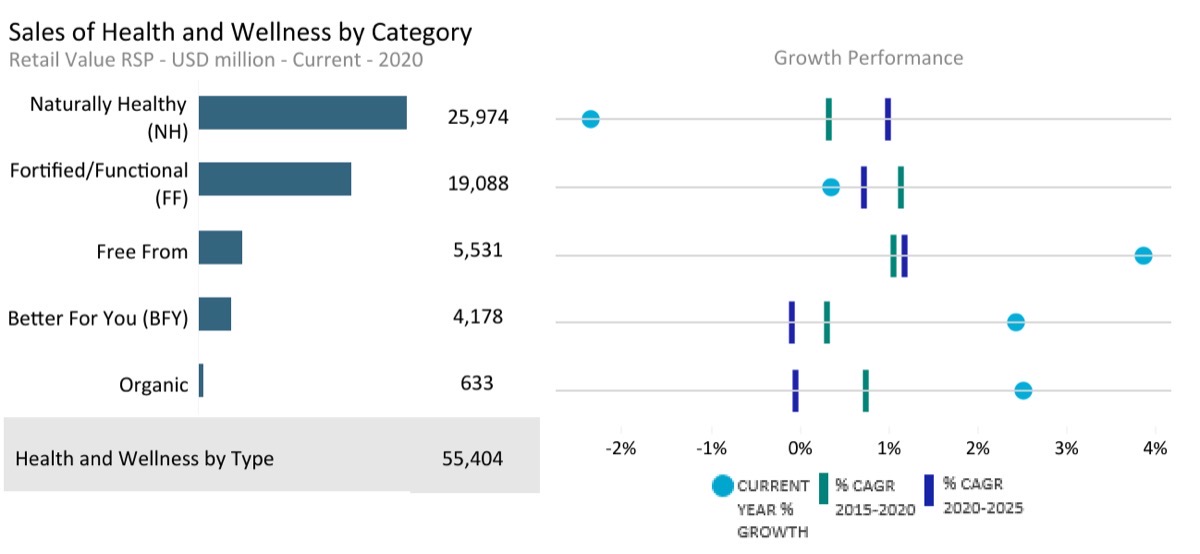

The retail value sales of health and wellness food and beverage products in Japan are expected to remain steady when comparing the compound annual growth rates from historic to forecast periods, i.e. (0.7% during 2015-2020 to 0.8% during 2020-2025). However, globally the category’s performance (retail value sales) is expected to slow down from a compound annual growth rate of 4.6% during 2015-2020 to 2.4% during 2020-2025.

- Sub-category breakdown

-

Current year growth in the above chart refers to the period 2019-20

Category

Unit

Market size (2020)

Retail value RSP

Forecast compound annual growth rate (2020/2025) %

Health and Wellness by Type

USD million

55,403.53

0.83

Better For You (BFY)

USD million

4,177.82

-0.09

Fortified/Functional (FF)

USD million

19,088.24

0.73

Free From

USD million

5,530.75

1.19

Naturally Healthy (NH)

USD million

25,973.68

1.00

Organic

USD million

633.05

-0.05

- Channel distribution

-

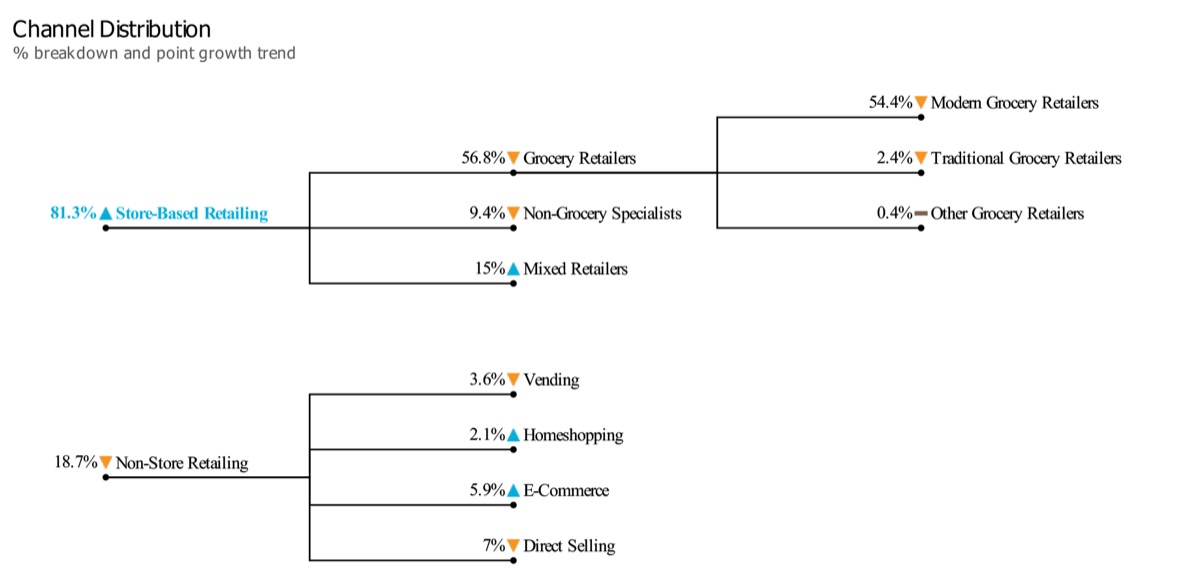

Note: The chart here showcases the retail value share of different channel sales for health and wellness by type products in Japan in 2020. The triangle/dash represents whether the specific channel share has increased/decreased or remained the same against its share in the previous year

- Market Insights

-

Market trends

- In 2020, both health and wellness packaged food and beverages witnessed opposite trends throughout the pandemic. Whilst health and wellness packaged food witnessed strong growth, health and wellness beverages recorded a strong decline. All health and wellness packaged food categories performed well primarily due to consumers’ greater health-consciousness and desire to improve their immunity to combat the virus. Meanwhile, within health and wellness beverages, only the niche category of organic beverages recorded growth. This was mainly due to a fall in on-the-go consumption and as most consumers had cut their expenditure in a difficult economic environment.

- Fortified/functional sports drinks have also been most negatively affected by the pandemic. In 2020, consumers were forced to refrain from various outdoor activities where such drinks were primarily consumed. The category’s demand is also highly dependent on the temperature conditions. A hot summer can lead to an increase in on-the-go consumption. In 2020, however, the weather conditions did not support the category’s growth, as Japan had an unusually long rainy season.

- Naturally healthy (NH) RTD tea, the largest category within NH beverages, had earlier witnessed strong growth over many years. However, due to the impact of the pandemic, in 2020, the category witnessed a strong decline in sales. NH RTD tea has long been a popular option for various occasions, such as at the office, at school and whilst on the go. However, COVID-19 led to the loss of such consumption occasions, which were replaced with drinking occasions at home. Some consumers shifted back to teabags for home consumption, as they are much more economical and better suited for bulk buying.

Prospects and growth opportunity

- FF (fortified/functional) beverages are expected to rebound in retail volume and value terms over the coming years, recovering some of the sales lost in 2020. Health awareness is likely to remain high amongst consumers due to fear of infection with COVID-19, which is expected to benefit the category’s growth. Consumers will have high demand for the easy intake of nutrition, especially products which enhance the immune system, such as lactic acid bacteria.

- Health awareness had already been a strong driver of growth for health and wellness packaged food and beverages over the review period. This trend will become even stronger in 2021 and beyond. Japanese consumers have become very particular about what they consume, including ingredients or products they should consume less of and vice versa. For this reason, the avoidance of sugar, calories or artificial sweeteners is likely to accelerate in the forecast period, which will, in turn, boost demand for NH (naturally healthy) beverages.

General health & wellness trends

- A degree of polarisation is expected to be seen amidst demand from Japanese consumers. Some consumers will be more budget-conscious due to the economic impact of measures taken to control COVID-19. On the other hand, others will continue to pay extra for products that claim to have health benefits due to the acceleration of health awareness due to the pandemic. This, in turn, will have a positive impact on most types of health and wellness, packaged food and beverages.

- In line with this, demand for healthy alternatives such as fibre is expected to grow. Consumers are paying more attention to fibre, although whole wheat products, such as bread, are found only in a limited number of shops. Instant noodles made with whole wheat are increasingly seen in the market, with big players such as Nissin Holdings and private label lines from major convenience store chains like 7-Eleven and Lawson offering instant noodles pouches and/or cups with whole wheat noodles for more fibre.

Retail Landscape

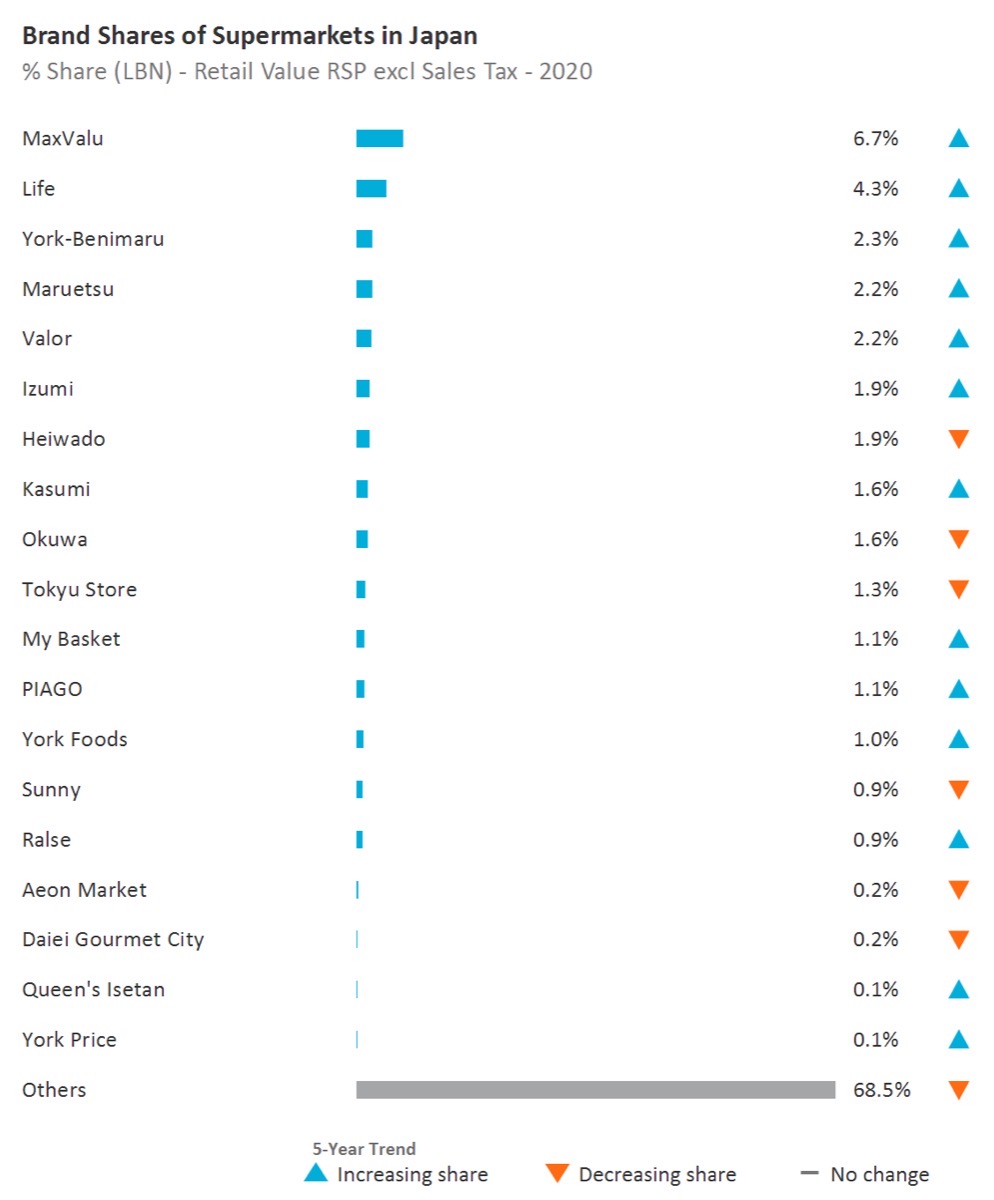

- Brand shares of supermarkets

-

Note: The 13th supermarket in the above chart is – Oliver’s The Delicatessen

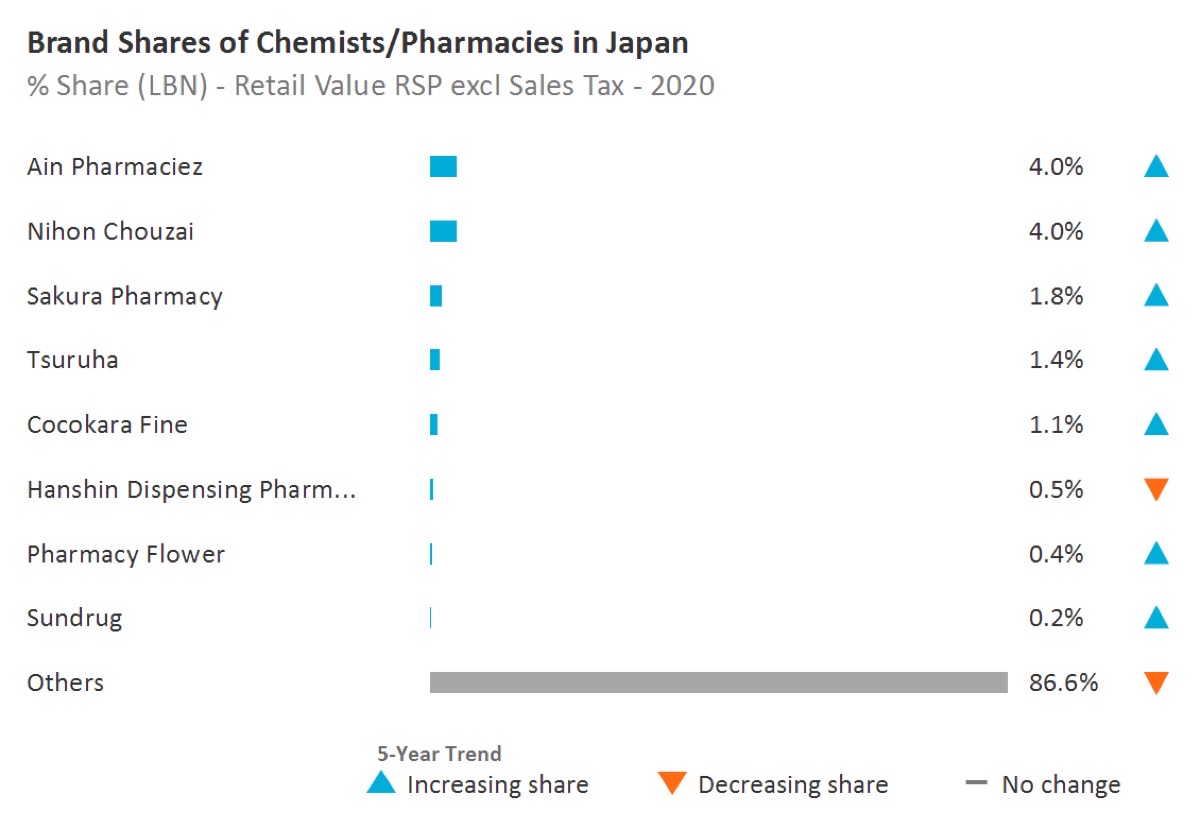

- Brand shares of chemists/pharmacies

-

Note: The 6th chemist/pharmacies in the above chart is – Hanshin Dispensing Pharmacy

- Retail insights

-

- COVID-19 had a significant impact on retailing in Japan in 2020. Overall value sales declined as consumers curbed their spending in response to the crisis. Despite this, supermarkets, the largest channel in value terms, witnessed stronger growth in 2020. This was largely due to the home seclusion seen in 2020, with the government advising against making non-essential trips outside the home. This saw consumers focus less on convenience and more on stockpiling supplies to eat or prepare meals at home. This resulted in an increase in the number of footfalls at supermarkets.

- One trend to grow out of COVID-19 was “nest egg consumption”, with this helping to drive dynamic growth in e-commerce in 2020. This trend refers to consumers who refrain from leaving their homes and instead shop online and carry out indoor activities for entertainment. One example was the increased demand for Nintendo Switch, which was in short supply for a long time due to increased demand and a decrease in production due to COVID-19. Demand increased for other items such as exercise video games, DVDs, craft supplies, and condiments, which consumers perceived could improve their home life.

- With consumers leading increasingly busy lives and many urban consumers lacking access to a car, the leading retailers are focusing on expanding their online services. For example, AEON Group, Ito-Yokado and Seiyu are all planning to strengthen their online supermarkets. AEON intends to establish an internet supermarket headquarters and an internet supermarket management company and open a large distribution centre in Chiba, Japan, in 2023 that will specialise in internet supermarkets.

- Chemists/pharmacies held a value (Retail value RSP excluding sales tax) market size of USD 56,784.3 million in n 2020. As a result, the channel’s compound annual growth rate for its value sales is expected to slightly slow down from historic (2015-2020: HCAGR: 0.9%) to its forecast period (2020-2025: FCAGR: 0.2%). Also, for 2020-2021, the channel witnessed a negative year on year growth (-3.3%) for its retail value sales.

- Definitions

- Acronyms Used & Key Notes

Definitions

|

Industry |

Category |

Definition |

|---|---|---|

|

Alcoholic Drinks |

Alcoholic Drinks |

Alcoholic drinks are the aggregation of beer, wine, spirits, cider/perry and RTDs. |

|

Alcoholic Drinks |

Beer |

An alcoholic drink usually brewed from malt, sugar, hops and water and fermented with yeast. Some beers are made by fermenting a cereal, especially barley, and therefore not flavoured by hops. Alcohol content for beer is varied – anything up to and over 14% ABV (alcohol by volume), although 3.5% to 5% is most common. Beer is the aggregation of lager, dark beer, stout and non/low alcohol beer. |

|

Alcoholic Drinks |

Cider/Perry |

Cider is made from fermented apple juice while perry is made from fermented pear juice. Both artisanal and industrial cider/perry are included. |

|

Alcoholic Drinks |

RTDs |

RTD stands for ‘ready-to-drink’. Other terms which may be used for these products are FABs, alcopops and premixes. The RTDs sector is the aggregation of malt-, wine-, spirit- and other types of premixed drinks. These drinks usually have an alcohol content of around 5% but this can reach as high as 10% ABV. Premixes containing a high percentage of alcohol of around 15%+ combined with juice or any other soft drink are included here. RTDs are usually marketed as products to be drunk neat, with ice, or as a cocktail ingredient. Fruit-flavoured, vodka-based spirits with an alcohol content of between 16-21% are classified here. Examples: Alizé, Ursus Roter, Berentzen Fruchtige, Kleiner Feigling. |

|

Alcoholic Drinks |

Spirits |

This is the aggregation of whisk(e)y, brandy and Cognac, white spirits, rum, tequila, liqueurs and other spirits. |

|

Alcoholic Drinks |

Wine |

This is the aggregation of still and sparkling light grape wines, fortified wine and vermouth and non-grape wine. In terms of alcohol content, light wine usually falls into the 8-14% ABV bracket while fortified wine ranges from 14-23% ABV. Low and non-alcoholic wine is also included in the data (attributed to each sector as appropriate). |

|

Beauty and Personal Care |

Skin Care |

This is the aggregation of facial care, body care, hand care and skin care sets/kits. |

|

Beauty and Personal Care |

Body Care |

This is the aggregation of firming/anti-cellulite products and general-purpose body care. |

|

Beauty and Personal Care |

Facial Care |

This is the aggregation of acne treatments, moisturisers and treatments, facial cleansers, toners, face masks, and lip care. Please note that Moisturisers and Treatments is the aggregation of basic moisturisers and anti-agers. |

|

Beauty and Personal Care |

Hand Care |

Includes all hand moisturisers, both premium and mass market, as well as combination hand and nail products. Includes protective emollients and deep moisturisers formulated to sooth and hydrate very dry or irritated skin, as well as those that prevent, or that are suitable for, eczema-prone or redness-prone skin. Excludes medicated emollients and/or those positioned as treatment for eczema or psoriasis. |

|

Beauty and Personal Care |

Skin Care Sets/Kits |

Multiple skin care items of the same brand line packaged together in a set and priced at an advantageous price compared to purchasing the items separately. Includes traditional gift sets, multi-step skin care regimens, skin care starter kits (including acne treatment regimen sets/kits) and skin care travel kits (sold through retail outlets). Also includes sets, which comprise of products from multiple categories (e.g. makeup and skin care), as long as the primary product is skin care. Men’s, women’s and unisex versions are included. Excludes: GWP (Gift with Purchase) – consumer does not pay for this (e.g. free product when you purchase a set or a free sample kit). |

|

Consumer Health |

Dietary Supplements |

It is the aggregation of all dietary supplements: Minerals, fish oils/omega fatty acids, garlic, ginseng, ginkgo biloba, evening primrose oil, Echinacea, St John's Wort, protein supplements, probiotic supplements, eye health supplements, co-enzyme Q10, glucosamine, combination herbal/traditional supplements, non-herbal/traditional supplements, and all other dietary supplements specific to country coverage. |

|

Consumer Health |

Paediatric Vitamins and Dietary Supplements |

All vitamin and dietary supplement products formulated, designed, marketed and labelled specifically for children. |

|

Consumer Health |

Tonics |

Include versions of combination dietary supplements that are sold in the format of liquid concentrates, mini-drinks, shots or oral gels. Include concentrated energy shot boosters and tonics such as 5-Hour Energy and Lipovitan. Exclude remedies made with active pharmaceutical ingredients as well as super fruit juice concentrates and weight-loss beverages, tracked under the Health and Wellness (HW) system. |

|

Consumer Health |

Vitamins |

This is the aggregation of multivitamins and single vitamins. |

|

Health and Wellness |

Health and Wellness by Type |

Health and Wellness by Type is the aggregation of all health and wellness food and beverages broken down by organic, fortified/functional, naturally healthy, better for you and free from products. |

|

Health and Wellness |

Better For You (BFY) |

Products where the amount of a substance considered to be less healthy (eg fat, sugar, salt, carbohydrates) has been actively reduced during production. To qualify for inclusion in this category, the “less healthy” element of the foodstuff needs to have been actively removed or substituted during the processing. This should also form a key part of the positioning/marketing of the product. Products which are naturally fat/sugar/carbohydrate -free are not included as nothing out of the ordinary has been done during their production to make them “better for you”. “No added sugar” claims are excluded too. Products most likely to be included here will be those which are low-fat/low-sugar versions of standard products (i.e. reduced fat mayonnaise, reduced fat cheese, reduced fat milk, reduced sugar confectionery, etc). |

|

Health and Wellness |

Fortified/Functional (FF) |

This category includes fortified/functional food and beverages. When identifying fortified/functional products, we focus on products to which health ingredients or/and nutrients have been added as well as brands that are positioned to deliver a certain functionality. To be included here the enhancement must be highlighted in the label or hold a health claim/nutritional claim. Fortified/functional food and beverages provide health benefits beyond their nutritional value and/or the level of added ingredients wouldn’t normally be found in that product. To merit inclusion in this category, the defining criterion here is that the product must have been actively fortified/enhanced during production. As such, inherently healthy products such as 100% fruit/vegetable juices are only included under "fortified/functional" if additional health ingredients (e.g. calcium, omega 3) have been added. To be included, the health benefit needs to form part of positioning/marketing of the product. For product category definitions please refer to the definitions section (can be found under the "Help" section on Passport) for the respective system: Packaged Food, Hot Drinks, Soft Drinks. |

|

Health and Wellness |

Free From |

This category includes free from gluten, free from lactose, free from allergens, free from dairy and free from meat products. This excludes foods which are certified ‘free’ of a specific product when this is based on use of sterilised equipment. |

|

Health and Wellness |

Naturally Healthy (NH) |

This category includes food and beverages based on naturally containing a substance that improves health and wellbeing beyond the product’s pure calorific value. These products are usually a healthier alternative within a certain sector/subsector. High fibre food (wholegrain/wholemeal/brown), soy products, sour milk drinks, nuts, seeds and trail mixes, honey, fruit and nut bars and olive oil are considered NH foods and 100% fruit/vegetable juice, superfruit juice, natural mineral water, spring water, RTD green tea etc. are considered NH beverages. While many of these products are marketed on a health basis, this might not always be the case. Naturally healthy food and beverages that are additionally fortified fall into the 'fortified/functional' category. |

|

Health and Wellness |

Organic |

Certified organic products are those which have been produced, stored, processed, handled and marketed in accordance with precise technical specifications (standards) and certified as "organic" by a certification body such as the Soil Association in the UK, the European Union or the US Department of Agriculture. It is important to note that an organic label applies to the production process, ensuring that the product has been produced and processed in an ecologically sound manner. The organic label is therefore a production process claim as opposed to a product quality claim. Note: For organic products to be included, the organic aspect needs to form a significant part of the overall positioning/marketing of the product, including the organic certification label in the packaging. |

|

Pet Care |

Dog and Cat Food |

This is the aggregation of dog and cat food. |

|

Pet Care |

Cat Food |

This is the aggregation of wet and dry cat food. |

|

Pet Care |

Cat Treats and Mixers |

This is the aggregation of mixers and treats for cats. |

|

Pet Care |

Dry Cat Food |

These products have a moisture content of 10-14% and are generally packed into paper, plastic or cardboard. Dry cat food is typically made from a combination of grain-based ingredients (corn and rice) and a meat component. It is typically produced by extrusion cooking under high heat and pressure and then sprayed with fat to increase palatability. Other ingredients may also be added to complete its composition. This is the aggregation of premium, mid-priced and economy dry cat food. Note: semi-moist food is included here. These products are extruded (combining meat and cereal), have a higher moisture content (20-40%) and are usually packaged in plastic or foil sachets. |

|

Pet Care |

Wet Cat Food |

These products have a moisture content of 60-85% and are generally (though not always) preserved by heat treatment. They are packaged in steel or aluminium cans, rigid or flexible plastic or semi-rigid aluminium trays. This is the aggregation of premium, mid-priced and economy wet cat food. |

|

Pet Care |

Dog Food |

This is the aggregation of wet and dry dog food. |

|

Pet Care |

Dog Treats and Mixers |

This is the aggregation of mixers and treats for dogs. |

|

Pet Care |

Dry Dog Food |

These products generally have a moisture content of 6-14% and are generally packed into paper, plastic or cardboard. Complete dry dog foods fall into two broad categories: Flaked (or 'Muesli' type blended products) and Extruded products (meat and cereals cooked by direct steaming). This is the aggregation of premium, mid-priced and economy dry dog food. Note: semi-moist food is included here. These products are extruded (combining meat and cereal) have a higher moisture content (20-40%) and are usually packaged in plastic or foil sachets. |

|

Pet Care |

Wet Dog Food |

These products have a moisture content of 60-85% and are generally (though not always) preserved by heat treatment. They are packaged in steel or aluminium cans, rigid or flexible plastic or semi-rigid aluminium trays. This is the aggregation of premium, mid-priced and economy wet dog food. |

|

Retail in Alcoholic Drinks |

Store-Based Retailing |

Store-based retailing is the aggregation of grocery retailers and non-grocery specialists and mixed retailers. |

|

Retail in Alcoholic Drinks |

Grocery Retailers |

Retailers selling predominantly food/beverages/tobacco and other everyday groceries. This is the aggregation of hypermarkets, supermarkets, discounters, convenience stores, independent small grocers, forecourt retailers, food/drink/tobacco specialists and other grocery retailers. |

|

Retail in Alcoholic Drinks |

Convenience Stores |

Chained grocery retail outlets selling a wide range of groceries and fitting several of the following characteristics: Extended opening hours •Selling area of less than 400 sq. metres •Located in residential neighbourhoods •Handling two or more of the following product categories: audio-visual goods (for sale or rent), foodservice (prepared take-away, made-to-order, and hot foods), newspapers or magazines, cut flowers or pot plants, greetings cards, automotive accessories. Example brands include 7-Eleven, Spar. |

|

Retail in Alcoholic Drinks |

Discounters |

Discounters are retail outlets typically with a selling space of between 400 and 2,500 square metres. Retailers' primary focus is on selling private label products within a limited range of food/beverages/tobacco and other groceries at budget prices. Discounters may also sell a selection of non-groceries, frequently as short-term special offers. Discounters can be classified as hard discounters and soft discounters. Hard discounter: first introduced by Aldi in Germany, and also known as limited-line discounters. Retail outlets, typically of 300-900 square metres, stocking fewer than 1,000 product lines, largely in packaged groceries. Goods are mainly private-label or budget brands. Soft discounter: usually slightly larger than hard discounters, and also known as extended-range discounters. Retail outlets typically stocking 1,000-4,000 product lines. As well as private-label and budget brands, stores commonly carry leading brands at discounted prices. Discounters excludes mass merchandisers and warehouse clubs. Example brands include Aldi, Lidl, Plus, Penny, Netto. |

|

Retail in Alcoholic Drinks |

Forecourt Retailers |

Grocery retail outlets selling a wide range of groceries from a gas station forecourt and fitting several of the following characteristics: • Extended opening hours • Selling area of less than 400 sq. metres • Handling two or more of the following product categories: audio-visual goods (for sale or rent), take-away food (readymade sandwiches, rolls or hot food), newspapers or magazines, cut flowers or pot plants, greetings cards, automotive accessories. Example brands include BP Connect, Shell Select. Forecourt retailers includes both chained forecourt retailers and independent forecourt retailers. |

|

Retail in Alcoholic Drinks |

Hypermarkets |

Hypermarkets are retail outlets with a selling space of over 2,500 square metres and with a primary focus on selling food/beverages/tobacco and other groceries. Hypermarkets also sell a range of non-grocery merchandise. Hypermarkets are frequently located on out-of-town sites or as the anchor store in a shopping centre. Example brands include Carrefour, Tesco Extra, Géant, E Leclerc, Intermarché, Auchan. Excludes cash and carry, warehouse clubs and mass merchandisers. |

|

Retail in Alcoholic Drinks |

Supermarkets |

Retail outlets selling groceries with a selling space of between 400 and 2,500 square metres. Excludes discounters, convenience stores and independent grocery stores. Example brands include Champion, Tesco, Casino. |

|

Retail in Alcoholic Drinks |

Food/drink/tobacco specialists |

Retail outlets specialising in the sale of mainly one category of food, drinks store and tobacconists. Includes bakers (bread and flour confectionery), butchers (meat and meat products), fishmongers (fish and seafood), greengrocers (fruit and vegetables), drinks stores (alcoholic and non-alcoholic drinks), tobacconists (tobacco products and smokers’ accessories), cheesemongers, chocolatiers and other single food categories. Alcoholic drinks stores are retail outlets with a primary focus on selling beer/wine/spirits/other alcoholic beverages. Example brands include: Threshers, Gall & Gall, Liquorland, Watson’s Wine Cellar |

|

Retail in Alcoholic Drinks |

Independent Small Grocers |

Retail outlets selling a wide range of predominantly grocery products. These outlets are usually not chained and if chained will have fewer than 10 retail outlets. Mainly family owned, often referred to as Mom and Pop stores. |

|

Retail in Alcoholic Drinks |

Other Grocery Retailers |

Other retailers selling predominantly food, beverages and tobacco or a combination of these. Includes kiosks, markets selling predominantly groceries. Includes CTNs and health food stores, Food & drink souvenir stores and regional speciality stores. Direct home delivery, eg of milk, meat from farm/dairy is excluded. Sari-Sari stores in Philippines and Warung (Waroon) in Indonesia, that can either be markets or kiosks, are included in Other grocery retailers unless they occupy a separate permanent outlet building, in which case they are included in Independent small grocers. Outlets located within wet markets, particularly in South East Asia (often located in government-owned multi-story buildings) should be counted as separate outlets. Wine sales from Vineyards are included here. |

|

Retail in Alcoholic Drinks |

Non-Grocery Specialists |

Retail outlets selling predominantly non-grocery consumer goods. Non-grocery retailers is the aggregation of: • Apparel and footwear specialist retailers • Electronics and appliance specialist retailers • Health & beauty specialist retailers • Home and garden specialist retailers • Leisure and personal goods specialist retailers • Other non-grocery retailers |

|

Retail in Alcoholic Drinks |

Drugstores/parapharmacies |

Retail outlets selling mainly OTC healthcare, cosmetics and toiletries, disposable paper products, household care products and other general merchandise. Such outlets may also offer prescription-bound medicines under the supervision of a pharmacist. Drugstores in Spain (Droguerias) also sell household cleaning agents, paint, DIY products and sometimes pet products and services such as photo processing. Example brands include Rossmann (Germany), Kruidvat (Netherlands), Walgreen’s (US), CVS (US), Medicine Shoppe (US), Matsumoto Kiyoshi (Japan), HAC Kimisawa (Japan). |

|

Retail in Alcoholic Drinks |

Mixed Retailers |

This is the aggregation of department stores, variety stores, mass merchandisers and warehouse clubs. |

|

Retail in Alcoholic Drinks |

Department Stores |

Outlets selling mainly non-grocery merchandise and at least five lines in different departments, usually with a sales area of over 2,500 sq metres. They are usually arranged over several floors. Example brands include Macy’s, Bloomingdale’s, Marks & Spencer, Harrods, Sears, JC Penney, Takashimaya, Mitsukoshi, Daimaru, Karstadt, Rinascente. |

|

Retail in Alcoholic Drinks |

Mass Merchandisers |

Mixed retail outlets that usually: (1) convey the image of a high-volume, fast-turnover outlet selling a variety of merchandise for less than conventional prices; (2) provide centralised check-out service; and (3) provide minimal customer assistance within each department. Example brands include Wal-Mart, Target and Kmart. Excludes hypermarkets and warehouse clubs/cash and carry stores. |

|

Retail in Alcoholic Drinks |

Variety Stores |

Non-grocery general merchandise outlets usually located on one floor, offering a wide assortment of extensively discounted fast-moving consumer goods on a self-service basis. Normally over 1,500 sq. metres in size, except in the case of dollar stores, these outlets give priority to fast-moving non-grocery items that have long shelf-lives. Includes catalogue showrooms and dollar stores. Example brands include Woolworth (Germany), Upim (Italy). |

|

Retail in Alcoholic Drinks |

Warehouse Clubs |

Warehouse Clubs are chained outlets that sell a wide variety of merchandise but do have a strong mix of both grocery and non-grocery products. Customers have to pay an annual membership fee in order to shop. The clubs are able to keep prices low due to the no-frills format of the stores and attempt to drive volume sales through aggressive pricing techniques. Warehouse Clubs typically: - exceed 2,500 sq. metres of selling space and are invariably -over 4,000 sq. metres in size; - convey the image of a high-volume, fast-turnover retailing at less than conventional prices; - provide minimal customer assistance within each department; and - are situated in out-of-town locations. Example brands include: - Costco - Sam’s Club (Wal-Mart) - PriceSmart - Cost-U-Less |

|

Retail in Alcoholic Drinks |

Non-Store Retailing |

The retail sale of new and used goods to the general public for personal or household consumption from locations other than retail outlets or market stalls. Non-store retailing is the aggregation of Vending, Direct Selling, Homeshopping and Internet Retailing. |

|

Retail in Alcoholic Drinks |

Direct Selling |

Direct selling is the marketing of consumer goods directly to consumers, generally in their homes or the homes of others, at their workplace and other places away from permanent retail locations. Direct selling occurs in two primary ways: one-to-one basis (usually by prior arrangement a demonstration is given by a direct seller to a customer) or party-plan basis (selling through explanation and demonstration of products to a group of prospective customers by a direct seller usually in the home of a host(ess) who invites other persons for this purpose). |

|

Retail in Alcoholic Drinks |

Homeshopping |

Homeshopping is the sale of consumer goods to the general public via mail order catalogues, TV shopping and direct mail. Consumers purchase goods in direct response to an advertisement or promotion through a mail item, printed catalogue, TV shopping programme, or Internet catalogue whereby the order is placed, and payment is made by phone, by post or through other media such as digital TV. Excludes sales on returned products/unpaid invoices. Excludes sales ordered and paid online which are instead included within Internet retailing. |

|

Retail in Alcoholic Drinks |

E-Commerce |

Sales of consumer goods to the general public via the Internet. Please note that this includes sales through mobile phones and tablets. Internet retailing includes sales generated through pure e-commerce web sites and through sites operated by store-based retailers. Sales data is attributed to the country where the consumer is based, rather than where the retailer is based. Also includes orders placed through the web for which payment is then made through a storecard, an online credit account subsequent to delivery or on delivery of the product. This payment may be by any mode of payment including postal cheque, direct debit, standing order or other banking tools. Includes orders paid for cash on delivery. Includes m-commerce: where consumers use smart phones or tablets to connect to Internet and purchase the goods online. |

|

Retail in Alcoholic Drinks |

Vending |

Vending means automatic retailing. It covers the sale of products and services at an unattended point of sale through a machine operated by introducing coins, bank notes, payment cards, tokens or other means of cashless payment. Coverage includes vending systems installed in public and semi-captive environments only. Hotels, transport networks, recreational centres, shopping centres/malls are included. Factories, offices, hospitals, prisons, schools and other captive environments are excluded. |

|

Retail in Beauty and Personal Care |

Store-Based Retailing |

Store-based retailing is the aggregation of grocery retailers and non-grocery specialists and mixed retailers. |

|

Retail in Beauty and Personal Care |

Grocery Retailers |

Retailers selling predominantly food/beverages/tobacco and other everyday groceries. This is the aggregation of hypermarkets, supermarkets, discounters, convenience stores, independent small grocers, forecourt retailers, food/drink/tobacco specialists and other grocery retailers. |

|

Retail in Beauty and Personal Care |

Modern Grocery Retailers |

Modern grocery retailing is the aggregation of those grocery channels that have emerged alongside the growth of chained retail: Hypermarkets, Supermarkets, Discounters, Forecourt Retailers and Convenience Stores. |

|

Retail in Beauty and Personal Care |

Convenience Stores |

Chained grocery retail outlets selling a wide range of groceries and fitting several of the following characteristics: Extended opening hours •Selling area of less than 400 sq. metres •Located in residential neighbourhoods •Handling two or more of the following product categories: audio-visual goods (for sale or rent), foodservice (prepared take-away, made-to-order, and hot foods), newspapers or magazines, cut flowers or pot plants, greetings cards, automotive accessories. Example brands include 7-Eleven, Spar. |

|

Retail in Beauty and Personal Care |

Discounters |

Discounters are retail outlets typically with a selling space of between 400 and 2,500 square metres. Retailers' primary focus is on selling private label products within a limited range of food/beverages/tobacco and other groceries at budget prices. Discounters may also sell a selection of non-groceries, frequently as short-term special offers. Discounters can be classified as hard discounters and soft discounters. Hard discounter: first introduced by Aldi in Germany, and also known as limited-line discounters. Retail outlets, typically of 300-900 square metres, stocking fewer than 1,000 product lines, largely in packaged groceries. Goods are mainly private-label or budget brands. Soft discounter: usually slightly larger than hard discounters, and also known as extended-range discounters. Retail outlets typically stocking 1,000-4,000 product lines. As well as private-label and budget brands, stores commonly carry leading brands at discounted prices. Discounters excludes mass merchandisers and warehouse clubs. Example brands include Aldi, Lidl, Plus, Penny, Netto. |

|

Retail in Beauty and Personal Care |

Forecourt Retailers |

Grocery retail outlets selling a wide range of groceries from a gas station forecourt and fitting several of the following characteristics: • Extended opening hours • Selling area of less than 400 sq. metres • Handling two or more of the following product categories: audio-visual goods (for sale or rent), take-away food (ready-made sandwiches, rolls or hot food), newspapers or magazines, cut flowers or pot plants, greetings cards, automotive accessories. Example brands include BP Connect, Shell Select. Forecourt retailers includes both chained forecourt retailers and independent forecourt retailers. |

|

Retail in Beauty and Personal Care |

Hypermarkets |

Hypermarkets are retail outlets with a selling space of over 2,500 square metres and with a primary focus on selling food/beverages/tobacco and other groceries. Hypermarkets also sell a range of non-grocery merchandise. Hypermarkets are frequently located on out-of-town sites or as the anchor store in a shopping centre. Example brands include Carrefour, Tesco Extra, Géant, E Leclerc, Intermarché, Auchan. Excludes cash and carry, warehouse clubs and mass merchandisers. |

|

Retail in Beauty and Personal Care |

Supermarkets |

Retail outlets selling groceries with a selling space of between 400 and 2,500 square metres. Excludes discounters, convenience stores and independent grocery stores. Example brands include Champion, Tesco, Casino. |

|

Retail in Beauty and Personal Care |

Traditional Grocery Retailers |

Traditional grocery retailing is the aggregation of those channels that are invariably non-chained and are, therefore, owned by families and/or run on an individual basis. Traditional grocery retailing is the aggregation of three channels: Independent Small Grocers, Food/Drink/Tobacco Specialists and Other Grocery Retailers. |

|

Retail in Beauty and Personal Care |

Non-Grocery Specialists |

Retail outlets selling predominantly non-grocery consumer goods. Non-grocery retailers is the aggregation of: • Apparel and footwear specialist retailers • Electronics and appliance specialist retailers • Health & beauty specialist retailers • Home and garden specialist retailers • Leisure and personal goods specialist retailers • Other non-grocery retailers |

|

Retail in Beauty and Personal Care |

Apparel and Footwear Specialist Retailers |

Outlets specialising in the sale of all types of apparel, footwear and fashion accessories including costume jewellery, belts, handbags, hats, scarves or a combination of these (for example stores selling handbags only are included). This includes those stores that carry a combination of all products for either men or women or children and those that may specialise by either gender, age or product. Example brands include Gap, H&M, Zara, C&A, Miss Selfridge, Foot Locker, Uniglo, Next, Matalan. Brands that offer sports apparel and sports goods are excluded from Apparel and footwear specialist retailers and are included in Sports goods stores. |

|

Retail in Beauty and Personal Care |

Electronics and Appliance Specialist Retailers |

Retail outlets specialising in the sale of large or small domestic electrical appliances, consumer electronic equipment (including mobile phones), computers or a combination of these. For mobile phone retailers, this excludes revenues derived from telecoms service plans and top-up cards, etc. Example brands include Apple, Best Buy, Euronics, PC World, Darty, But, Media Markt, Yamada Denki, Gome (China). |

|

Retail in Beauty and Personal Care |

Health and Beauty Specialist Retailers |

This is the aggregation of chemists/pharmacies, drugstores/parapharmacies, beauty specialist retailers, optical goods stores and other healthcare specialist retailers. |

|

Retail in Beauty and Personal Care |

Beauty Specialist Retailers |

Beauty specialist retailers are chained or independent retail outlets with a primary focus on selling fragrances, other cosmetics and toiletries, beauty accessories or a combination of these. Examples of Beauty specialist retailer brands include: Body Shop, Marionnaud, Sephora and Bath and Body Works. |

|

Retail in Beauty and Personal Care |

Chemists/Pharmacies |

Retail outlets selling prescription-bound medicines under the supervision of a pharmacist and as its core activity (other activities include sales of OTC healthcare and cosmetics and toiletries products). |

|

Retail in Beauty and Personal Care |

Drugstores/parapharmacies |

Retail outlets selling mainly OTC healthcare, cosmetics and toiletries, disposable paper products, household care products and other general merchandise. Such outlets may also offer prescription-bound medicines under the supervision of a pharmacist. Drugstores in Spain (Droguerias) also sell household cleaning agents, paint, DIY products and sometimes pet products and services such as photo processing. Example brands include Rossmann (Germany), Kruidvat (Netherlands), Walgreen’s (US), CVS (US), Medicine Shoppe (US), Matsumoto Kiyoshi (Japan), HAC Kimisawa (Japan). |

|

Retail in Beauty and Personal Care |

Home and Garden Specialist Retailers |

This is the aggregation of homewares and home furnishing stores and home improvement and gardening stores. Business-to-business sales are excluded. Home improvement and gardening stores are chained or independent retail outlets with a primary focus on selling one or more of the following categories: Home improvement materials and hardware, Paints, coatings and wall coverings, Kitchen and bathroom, fixtures and fittings, Gardening equipment, House/Garden plants. Home improvement and gardening stores includes Home improvement centres / DIY stores, Hardware stores (Ironmongers), Garden centres, Kitchen and bathroom showrooms, Tile specialists, Flooring specialists. Homewares and Home Furnishing stores are retail outlets specialising in the sale of home furniture and furnishings, homewares, floor coverings, soft furnishings, lighting etc. |

|

Retail in Beauty and Personal Care |

Homewares and Home Furnishing Stores |

Retail outlets specialising in the sale of home furniture and furnishings, homewares, floor coverings, soft furnishings, lighting etc. |

|

Retail in Beauty and Personal Care |

Other Non-Grocery Specialists |

Other non-grocery retailers are chained or independent retail outlets, kiosks, market stalls or street vendors and with a primary focus on selling non-food merchandise. Other non-grocery retailers include Charity shops, Second-hand shops and Market stalls. |

|

Retail in Beauty and Personal Care |

Outdoor Markets |

Includes bazaars, kiosks, street vendors and beach vendors. |

|

Retail in Beauty and Personal Care |

Mixed Retailers |

This is the aggregation of department stores, variety stores, mass merchandisers and warehouse clubs. |

|

Retail in Beauty and Personal Care |

Department Stores |

Outlets selling mainly non-grocery merchandise and at least five lines in different departments, usually with a sales area of over 2,500 sq metres. They are usually arranged over several floors. Example brands include Macy’s, Bloomingdale’s, Marks & Spencer, Harrods, Sears, JC Penney, Takashimaya, Mitsukoshi, Daimaru, Karstadt, Rinascente. |

|

Retail in Beauty and Personal Care |

Mass Merchandisers |

Mixed retail outlets that usually: (1) convey the image of a high-volume, fast-turnover outlet selling a variety of merchandise for less than conventional prices; (2) provide centralised check-out service; and (3) provide minimal customer assistance within each department. Example brands include Wal-Mart, Target and Kmart. Excludes hypermarkets and warehouse clubs/cash and carry stores. |

|

Retail in Beauty and Personal Care |

Variety Stores |

Non-grocery general merchandise outlets usually located on one floor, offering a wide assortment of extensively discounted fast-moving consumer goods on a self-service basis. Normally over 1,500 sq. metres in size, except in the case of dollar stores, these outlets give priority to fast-moving non-grocery items that have long shelf-lives. Includes catalogue showrooms and dollar stores. Example brands include Woolworth (Germany), Upim (Italy). |

|

Retail in Beauty and Personal Care |

Warehouse Clubs |

Warehouse Clubs are chained outlets that sell a wide variety of merchandise but do have a strong mix of both grocery and non-grocery products. Customers have to pay an annual membership fee in order to shop. The clubs are able to keep prices low due to the no-frills format of the stores and attempt to drive volume sales through aggressive pricing techniques. Warehouse Clubs typically: - exceed 2,500 sq. metres of selling space and are invariably -over 4,000 sq. metres in size; - convey the image of a high-volume, fast-turnover retailing at less than conventional prices; - provide minimal customer assistance within each department; and - are situated in out-of-town locations. Example brands include: - Costco - Sam’s Club (Wal-Mart) - PriceSmart - Cost-U-Less |

|

Retail in Beauty and Personal Care |

Non-Store Retailing |

The retail sale of new and used goods to the general public for personal or household consumption from locations other than retail outlets or market stalls. Non-store retailing is the aggregation of Vending, Direct Selling, Homeshopping and Internet Retailing. |

|

Retail in Beauty and Personal Care |

Direct Selling |

Direct selling is the marketing of consumer goods directly to consumers, generally in their homes or the homes of others, at their workplace and other places away from permanent retail locations. Direct selling occurs in two primary ways: one-to-one basis (usually by prior arrangement a demonstration is given by a direct seller to a customer) or party-plan basis (selling through explanation and demonstration of products to a group of prospective customers by a direct seller usually in the home of a host(ess) who invites other persons for this purpose). |

|

Retail in Beauty and Personal Care |

Homeshopping |

Homeshopping is the sale of consumer goods to the general public via mail order catalogues, TV shopping and direct mail. Consumers purchase goods in direct response to an advertisement or promotion through a mail item, printed catalogue, TV shopping programme, or Internet catalogue whereby the order is placed, and payment is made by phone, by post or through other media such as digital TV. Excludes sales on returned products/unpaid invoices. Excludes sales ordered and paid online which are instead included within Internet retailing. |

|

Retail in Beauty and Personal Care |

E-Commerce |

Sales of consumer goods to the general public via the Internet. Please note that this includes sales through mobile phones and tablets. Internet retailing includes sales generated through pure e-commerce web sites and through sites operated by store-based retailers. Sales data is attributed to the country where the consumer is based, rather than where the retailer is based. Also includes orders placed through the web for which payment is then made through a storecard, an online credit account subsequent to delivery or on delivery of the product. This payment may be by any mode of payment including postal cheque, direct debit, standing order or other banking tools. Includes orders paid for cash on delivery. Includes m-commerce: where consumers use smart phones or tablets to connect to Internet and purchase the goods online. |

|

Retail in Beauty and Personal Care |

Vending |

Vending means automatic retailing. It covers the sale of products and services at an unattended point of sale through a machine operated by introducing coins, bank notes, payment cards, tokens or other means of cashless payment. Coverage includes vending systems installed in public and semi-captive environments only. Hotels, transport networks, recreational centres, shopping centres/malls are included. Factories, offices, hospitals, prisons, schools and other captive environments are excluded. |

|

Retail in Beauty and Personal Care |

Hair Salons |

Hair salons |

|

Retail in Health and Wellness |

Store-Based Retailing |

Store-based retailing is the aggregation of grocery retailers and non-grocery specialists and mixed retailers. |

|

Retail in Health and Wellness |

Convenience Stores |

Chained grocery retail outlets selling a wide range of groceries and fitting several of the following characteristics: Extended opening hours •Selling area of less than 400 sq. metres •Located in residential neighbourhoods •Handling two or more of the following product categories: audio-visual goods (for sale or rent), foodservice (prepared take-away, made-to-order, and hot foods), newspapers or magazines, cut flowers or pot plants, greetings cards, automotive accessories. Example brands include 7-Eleven, Spar. |

|

Retail in Health and Wellness |

Discounters |

Discounters are retail outlets typically with a selling space of between 400 and 2,500 square metres. Retailers' primary focus is on selling private label products within a limited range of food/beverages/tobacco and other groceries at budget prices. Discounters may also sell a selection of non-groceries, frequently as short-term special offers. Discounters can be classified as hard discounters and soft discounters. Hard discounter: first introduced by Aldi in Germany, and also known as limited-line discounters. Retail outlets, typically of 300-900 square metres, stocking fewer than 1,000 product lines, largely in packaged groceries. Goods are mainly private-label or budget brands. Soft discounter: usually slightly larger than hard discounters, and also known as extended-range discounters. Retail outlets typically stocking 1,000-4,000 product lines. As well as private-label and budget brands, stores commonly carry leading brands at discounted prices. Discounters excludes mass merchandisers and warehouse clubs. Example brands include Aldi, Lidl, Plus, Penny, Netto. |

|

Retail in Health and Wellness |

Forecourt Retailers |

Grocery retail outlets selling a wide range of groceries from a gas station forecourt and fitting several of the following characteristics: • Extended opening hours • Selling area of less than 400 sq. metres • Handling two or more of the following product categories: audio-visual goods (for sale or rent), take-away food (ready made sandwiches, rolls or hot food), newspapers or magazines, cut flowers or pot plants, greetings cards, automotive accessories. Example brands include BP Connect, Shell Select. Forecourt retailers includes both chained forecourt retailers and independent forecourt retailers. |

|

Retail in Health and Wellness |

Hypermarkets |

Hypermarkets are retail outlets with a selling space of over 2,500 square metres and with a primary focus on selling food/beverages/tobacco and other groceries. Hypermarkets also sell a range of non-grocery merchandise. Hypermarkets are frequently located on out-of-town sites or as the anchor store in a shopping centre. Example brands include Carrefour, Tesco Extra, Géant, E Leclerc, Intermarché, Auchan. Excludes cash and carry, warehouse clubs and mass merchandisers. |

|

Retail in Health and Wellness |

Supermarkets |

Retail outlets selling groceries with a selling space of between 400 and 2,500 square metres. Excludes discounters, convenience stores and independent grocery stores. Example brands include Champion, Tesco, Casino. |

|

Retail in Health and Wellness |

Independent Small Grocers |

Retail outlets selling a wide range of predominantly grocery products. These outlets are usually not chained and if chained will have fewer than 10 retail outlets. Mainly family owned, often referred to as Mom and Pop stores. |

|

Retail in Health and Wellness |

Other Grocery Retailers |

Other retailers selling predominantly food, beverages and tobacco or a combination of these. Includes kiosks, markets selling predominantly groceries. Includes CTNs and health food stores, Food & drink souvenir stores and regional speciality stores. Direct home delivery, e.g. of milk, meat from farm/dairy is excluded. Sari-Sari stores in Philippines and Warung (Waroon) in Indonesia, that can either be markets or kiosks, are included in Other grocery retailers unless they occupy a separate permanent outlet building, in which case they are included in Independent small grocers. Outlets located within wet markets, particularly in South East Asia (often located in government-owned multi-story buildings) should be counted as separate outlets. Wine sales from Vineyards are included here. |

|

Retail in Health and Wellness |

Non-Store Retailing |

The retail sale of new and used goods to the general public for personal or household consumption from locations other than retail outlets or market stalls. Non-store retailing is the aggregation of Vending, Direct Selling, Homeshopping and Internet Retailing. |

|

Retail in Health and Wellness |

Vending |

Vending means automatic retailing. It covers the sale of products and services at an unattended point of sale through a machine operated by introducing coins, bank notes, payment cards, tokens or other means of cashless payment. Coverage includes vending systems installed in public and semi-captive environments only. Hotels, transport networks, recreational centres, shopping centres/malls are included. Factories, offices, hospitals, prisons, schools and other captive environments are excluded. |

|

Retail in Health and Wellness |

Homeshopping |

Homeshopping is the sale of consumer goods to the general public via mail order catalogues, TV shopping and direct mail. Consumers purchase goods in direct response to an advertisement or promotion through a mail item, printed catalogue, TV shopping programme, or Internet catalogue whereby the order is placed, and payment is made by phone, by post or through other media such as digital TV. Excludes sales on returned products/unpaid invoices. Excludes sales ordered and paid online which are instead included within Internet retailing. |

|

Retail in Health and Wellness |

E-Commerce |

Sales of consumer goods to the general public via the Internet. Please note that this includes sales through mobile phones and tablets. Internet retailing includes sales generated through pure e-commerce web sites and through sites operated by store-based retailers. Sales data is attributed to the country where the consumer is based, rather than where the retailer is based. Also includes orders placed through the web for which payment is then made through a storecard, an online credit account subsequent to delivery or on delivery of the product. This payment may be by any mode of payment including postal cheque, direct debit, standing order or other banking tools. Includes orders paid for cash on delivery. Includes m-commerce: where consumers use smart phones or tablets to connect to Internet and purchase the goods online. |

|

Retail in Health and Wellness |

Direct Selling |

Direct selling is the marketing of consumer goods directly to consumers, generally in their homes or the homes of others, at their workplace and other places away from permanent retail locations. Direct selling occurs in two primary ways: one-to-one basis (usually by prior arrangement a demonstration is given by a direct seller to a customer) or party-plan basis (selling through explanation and demonstration of products to a group of prospective customers by a direct seller usually in the home of a host(ess) who invites other persons for this purpose). |

|

Retail in Pet Care |

Store-Based Retailing |

Store-based retailing is the aggregation of grocery retailers and non-grocery specialists and mixed retailers. |

|

Retail in Pet Care |

Grocery Retailers |